The ABCs of Cryptocurrency and Non-Fungible Tokens (“NFTs”)

03 August, 2022

03 August, 2022-

Richard Tam

Richard Tam -

Canada

Canada

Bitcoin. Ethereum. Litecoin. Dogecoin. NFTs.

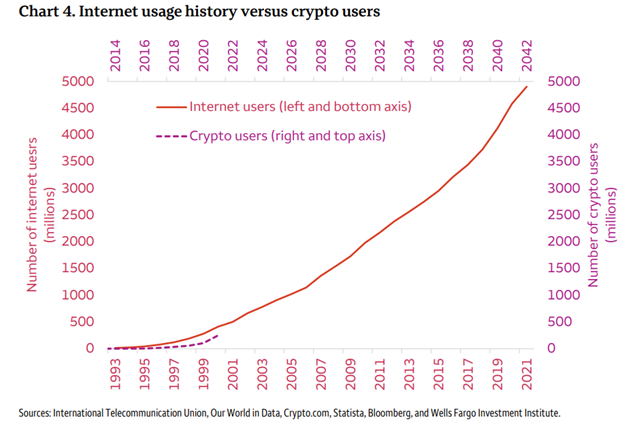

While they may seem like buzzwords or fads, cryptocurrencies or digital assets are experiencing a similar adoption pattern to the internet in the 1990s. In 1995, 14% of U.S. adults had internet access; by 2000, that rate increased to 46%.[1]

In the past 12 months, 13% of Americans had bought or traded cryptocurrencies, which means we may be entering the hyper adoption phase of cryptocurrencies.[2] This point is illustrated below as the number of crypto users are closely following the number of internet users:[3]

This rapid expansion has also led to a rise in fraudulent activity with digital assets (e.g. Ponzi schemes, money laundering, etc.).

In this article, we will provide some background on cryptocurrencies, share a few of the digital asset crimes that have occurred and outline several fraud prevention strategies and mitigation tactics to safeguard your assets.

Background

In 2008, someone with the pseudonym Satoshi Nakamoto published a white paper called “Bitcoin: A Peer-to-Peer Electronic Cash System”, which outlined the blockchain network. Blockchain is a form of record-keeping; it is a digital ledger. On January 3, 2009, Bitcoin (“BTC”) officially launched.[4]

On May 22, 2010, the first commercial transaction occurred when Laszlo Hanyecz purchased two Papa John’s pizzas for 10,000 BTC (on May 22, 2021, the 11th anniversary, 1 BTC = $63,000 USD; therefore, the two pizzas = $630M USD). In this transaction, the data would have been sent to Bitcoin’s decentralized network of nodes. Nodes verify, approve, and store data; once validated, the transaction is grouped with others to create a block and added to a chain of transactions (hence blockchain).[5] That block is encrypted and the transaction is permanent.

Since then, various exchanges have been created to buy and sell bitcoin and other tokens, such as Ethereum and Litecoin which have been developed as alternatives.

Cryptocurrency is a digital or virtual currency that exists in a secure database. It is an alternative to fiat, or government-issued, currency (e.g. Canadian dollar). Cryptocurrencies are also decentralized, which removes intermediaries (e.g. banks or monetary institutions). By eliminating the intermediary, fund transfers are comparatively faster to fiat transactions and are secured by using public or private keys.

Unfortunately, the use of these digital assets have become popular with criminals.

Scams

One of the largest Canadian crypto frauds involves QuadrigaCX, a cryptocurrency exchange, which the Ontario Securities Commission described as: “an old-fashioned fraud wrapped in modern technology.”[6] QuadrigaCX’s co-founder and CEO Gerald Cotton committed fraud by using QuadrigaCX’s trading platform to create a Ponzi scheme and misappropriate assets for personal use. On February 5, 2019, QuadrigaCX filed for creditor protection as over 76,000 clients were owed in excess of $215M CAD in assets.

According to the British Columbia Royal Canadian Mounted Police (“BC RCMP”), the number of fraud reports involving cryptocurrencies has increased exponentially from 734 in 2017 to 7,596 for the first 8 months of 2020. In the first 8 months of 2020, Canadians lost approximately $11M CAD from digital currency scams.[7]

In February 2022, two individuals were arrested in the United States for an alleged conspiracy to launder cryptocurrency that was stolen in 2016, currently valued at roughly $4.5B USD. It is alleged that these individuals used money laundering techniques such as creating fictitious identities, depositing stolen funds into various accounts on virtual currency exchanges and darknet markets and withdrawing the funds to distort the flow of transactions, etc.[8]

In addition to money laundering, fraudsters have been using “rug pulls”[9] of various NFT projects to scam over $2.8B from individuals in 2021.[10]

NFTs are unique crypto assets that cannot be replicated or replaced (i.e. NFTs claim to have a proof of ownership). NFTs include digital items such as images, videos, virtual land, etc. They are speculative and popular with sales reaching $25B USD in 2021.[11]

As an example, it is alleged that De’Aaron Fox, a professional basketball player for the Sacramento Kings, used the “rug pull” technique to siphon $1.2M from investors.[12] He backed a venture in December 2021 where fans could purchase a NFT with the promise of potential benefits such as tickets and merchandise; however, shortly after the money was raised, the project was cancelled (i.e. the investors’ assets were worthless).

Fraud Prevention Strategies

We have outlined several tips to consider when handling digital assets:

- Although cryptocurrencies such as bitcoin are a medium of exchange (i.e. these digital coins can be used to obtain other goods and services), be aware that Canadian government agencies or police do not accept payment of cryptocurrency, gift cards, etc.

- As with any potential investment, especially speculative investments such as NFTs, research and perform your due diligence to assess your risk tolerance and analyze the project’s feasibility.

- To protect your digital assets, it is recommended that you use a cold wallet (i.e. a hardware wallet that is not connected to the internet), use secure internet when making cryptocurrency transactions, maintain multiple wallets to diversify your portfolio and change your passwords to these accounts periodically.[13]

- Be careful when transferring crypto assets. As there is no intermediary, it is unlikely that a transaction (whether by mistake or a fraudulent error) will be reversed.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

- ibid

- Chart 4 is from Wells Fargo Investment Institute’s Special Report on Understanding Cryptocurrency – February 2022: https://saf.wellsfargoadvisors.com/emx/dctm/Research/wfii/wfii_reports/Investment_Strategy/cryptocurrency020722.pdf

- ibid

- A “rug pull” is a scam where developers initially pump or hype up a NFT project to draw more investments from individuals. Then the developers abandon the project and removes any liquidity (i.e. the investors lose all of their money).

Richard Tam

BComm, GDA, CPA, CA, CFE, Senior Manager/Vice President

- +1 613.389.3176

- rtam@mdd.com

- Kingston, ON, Canada

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Beyond the Fraud Triangle: Navigating Fraud Risks in Today’s Business Landscape

FRAUD. A five-letter word with consequential effects on individuals, organizations, and the economy as a whole. Fraud can be defined as an intentional act of deception in order to acquire something of value, whether it be a personal or financial...

How to Tackle Employee Fraud

Picture this, you, CFO, are sitting at your desk when an anonymous letter arrives alleging that employee X has been committing fraud against your company. Your first thoughts might be disbelief, anger and betrayal. You may question your relationship with...

Fraud Fighting 101

While I consider myself a pacifist, as a forensic accountant, I have been occasionally referred to as a fraud “fighter”. So, in the spirit of International Fraud Awareness Week (November 13 to 19, 2022), I would like to share some...

Ghosts, Ghouls and Cyber Claims

We usually think of Hallowe’en when October rolls around; however, did you know that October is also cyber security awareness month? NetDiligence recently released the 12th iteration of their Cyber Claims Study. They analyzed approximately 7,500 cyber claims from period...

")

The ABCs of Cryptocurrency and Non-Fungible Tokens (“NFTs”)

Bitcoin. Ethereum. Litecoin. Dogecoin. NFTs. While they may seem like buzzwords or fads, cryptocurrencies or digital assets are experiencing a similar adoption pattern to the internet in the 1990s. In 1995, 14% of U.S. adults had internet access; by 2000,...

COVID-19 and Fraud Claims

COVID-19 has sent shockwaves throughout much of the insurance world. Insurance company stocks have been some of the worst performing since the virus went, well… viral, in anticipation of declines in profits due in part to COVID-related claims. Much of...

Fraud in the time of COVID-19: Proactive steps to mitigate fraud risk

As the markets react to each update on COVID-19, a quote from Warren Buffet has seen increased circulation: “Only when the tide goes out do you see who’s been swimming naked”. The current environment has seen increasing news of corporate...

“Frenemies”: Is your organisation in bed with Brutus?

A growing area of concern for corporates is the proportion of fraud committed by “frenemies”, an encompassing term for the third parties a company works with on a day-to-day basis. This includes suppliers, agents and consumers: entities with which a...

The Better Way – Tips For Implementing Controls To Prevent Fraud

Last week, the Auditor General of Toronto issued a report estimating that in 2018 alone, the TTC lost $61 million due to fare evasion. As both a frequent rider of the TTC and a forensic accountant specializing in fraud investigations, I...

Fraud and Corruption: How Culture Impacts Effective Risk Management

The Fraud Triangle: Rationalisation, Opportunity and Pressure Any elementary student of fraud will be aware of the “Fraud Triangle”, a theory developed by Edwin Sutherland and Donald Cressey. This theory posits three elements of fraud: Rationalisation (the ability of the...

Fidelity / Fraud Losses: Forensic Investigation and Loss Quantification Concepts

A fraudster’s gain is someone else’s pain – or loss; but is the corporate fraudster’s gain always the same as the insured’s financial loss? Are the financial implications of the fraud always the same as the actual loss to an...

Quantifying Damages in Negligence Cases Involving Banks, Lenders

Banks rely on various professionals to help them assess the financial health of their borrowers. But sometimes these professionals make mistakes. As experts in quantifying economic damage, we at MDD are often asked to quantify the losses sustained by lenders...

How to Protect Your Business Assets – What You Should Know

The most common response I hear from business owners who are victims of employee fraud is “I never thought this would happen to me”. Employee theft, especially in the automotive industry, is common, because small businesses such as car dealerships...

3 Tips On How To Protect Your Firm From Fraud & Internet Theft

While we’re thinking about turkey and cranberry, an important business holiday will come and go – not with the same fanfare as Thanksgiving perhaps but with significant potential for preserving the business future for those who take note. During International...

Foreign Exchange Issues in Damage Quantification: Part II – Applying the Concepts

In the previous post, we presented a basic framework for analyzing the impact of foreign exchange fluctuations on quantifying financial remedies. We argued that the treatment of foreign exchange should be consistent with the principal underlying the financial remedy being awarded;...

Foreign Exchange Issues in Damage Quantification: Part I – Basic Concepts

International trade is an increasingly important part of the Canadian economy, as this picture clearly shows: As a result, it is not uncommon for litigation to involve the quantification of financial remedies across multiple political and monetary boundaries. How does...

Mining Industry Revisits Anti-Corruption Procedures

Mining companies should take note of Canada’s stricter penalties and more aggressive enforcement of anti-corruption laws and make sure their anti-bribery compliance procedures are up to speed, lawyers, forensic accountants and mining executives warned at a recent conference in Toronto....

Cheque Fraud – Who Is Responsible?

When a business falls victim to cheque fraud, it may look to its bank for recovery for allowing the fraudulent cheques to be cashed. In some recent cases, banks have been found liable and have been required to make whole...

Assessing Financial Motive

It is alleged that your client had financial motive to commit a very serious crime. Forensic accountants are often utilized to analyze the defendant’s financial records, and provide an opinion on the existence of financial circumstances that assist in assessing...

Accounting Fraud, Occupational Fraud & Abuse – A Clear & Present Danger to Your Business

The U.S. Chamber of Commerce estimates that occupational fraud costs U.S. businesses over $50 billion annually and that one-third of business failures are directly related to employee theft. The Chamber also estimates that 75% of all employees have stolen from...

Benford’s Law: A Powerful Tool for Uncovering Fraudulent Financial Transactions

Usually when you tell people that you’re a forensic accountant, you’re met with the same predictable and equally awful response: “So, you count dead peoples’ money?” Well, not exactly. It’s generally followed by something like, “You must be really good...

Accounting For Attorneys

It is becoming increasingly important for attorneys to understand financial statements and their relevance to various types of business and legal situations. The non-accountant attorney will greatly benefit from a basic understanding of the key principles of accounting. Equally important...

Financial Statements are Friends not Foes

Discovery is under-way. The records are starting to flow. As you leaf through a box of documents just delivered, you pull out a stack of financial statements and, like so many other attorneys, you cringe. As you scan through the...

Are Risks Hiding in the way your Revenues and “Expenses” are Reported?

Are you concerned about how your employees can get around your accounting policies or what unintended impact they might have? Here are two areas where accounting policies may pose a risk. Revenue Recognition Revenue recognition is always on the mind...

5 Steps to Investigating Fidelity Claims

Fidelity losses are difficult to investigate because frauds can be complex and hard to detect. Here are 5 steps to keep in mind when assessing fidelity claims. Understand business and accounting system Identify who performs the accounting duties and the documents generated...

Forensic Accountants Make It Add Up

Corporate fraud, insider trading, 9/11, intellectual property infringement the list goes on as to instances where parties have committed acts resulting in financial losses. The legal challenge in proving financial wrongdoing is a minefield in itself, but what steps need...