Natural Gas – The Past, Present and Future

11 March, 2024

11 March, 2024-

Nattakarn Prasitsumrit, Kent Bogdan

Nattakarn Prasitsumrit, Kent Bogdan

There has been a significant push towards transitioning to cleaner and renewable energy sources, moving away from fossil fuels due to their environmental impact. By looking at the past, the present and the future, the question remains: can we realistically achieve a complete phase-out of fossil fuels.?

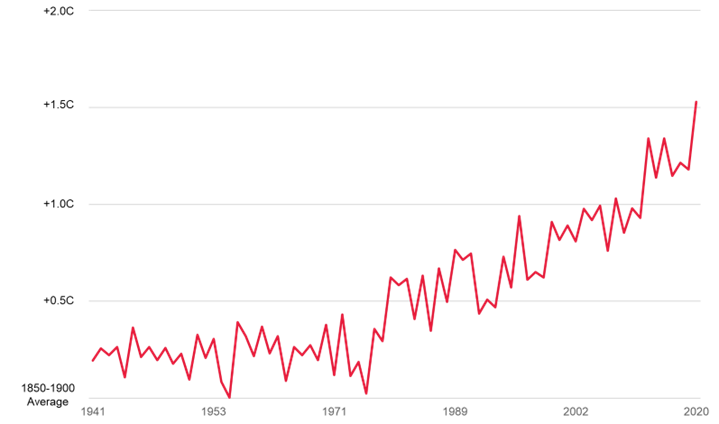

Why is the energy transition important? This chart illustrates for the first time, global warming has exceeded the critical threshold of 1.5°C across an entire year from February 2023 to January 2024. Even though the world has not yet permanently breached the 1.5°C threshold target outlined in the 2015 Paris climate agreement, which is measured over decades, this emphasises the urgency of expediting the energy transition.

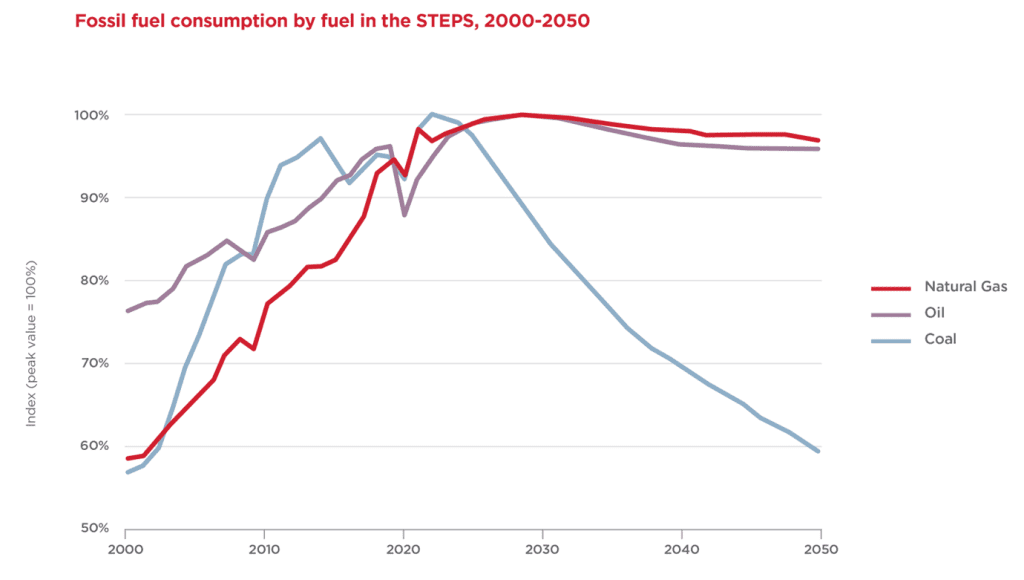

Despite the urgent need for a clean energy transition, the consumption of all three fossil fuels is projected to increase and peak by 2030, based on current government policy under the Stated Policies Scenarios (“STEPS”). Although global coal demand is expected to decline sharply after the peak, natural gas and crude oil, with relatively lower carbon emissions, are forecasted to decline more gradually. However, these projected declines are inconsistent with the requirements of the Net Zero Emissions (“NZE”) scenario.

In this briefing, we will focus on natural gas, which has cleaner combustion compared to coal and oil. Natural gas emits about 50% less carbon dioxide when burned than coal and is expected to remain a key component in the energy mix for decades, even amid ongoing efforts towards green transition.

The growth seen in natural gas consumption is matched by a substantial upward trend in production since 2000, almost doubling from 2010 to the present, with the US taking the lead, followed by Russia.

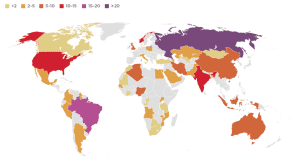

Natural gas production is expected to keep increasing as many countries are still actively developing new gas fields. This chart shows 47 countries with approved plans for new oil and gas fields, that have received final investment decisions for development. Currently, Russia has the largest gas reserve, followed by Iran, Qatar and the US.

In addition to the approved new gas fields, there has been significant recent news about new gas discoveries worldwide in locations such as Turkey, Indonesia, Morocco, Bangladesh and more.

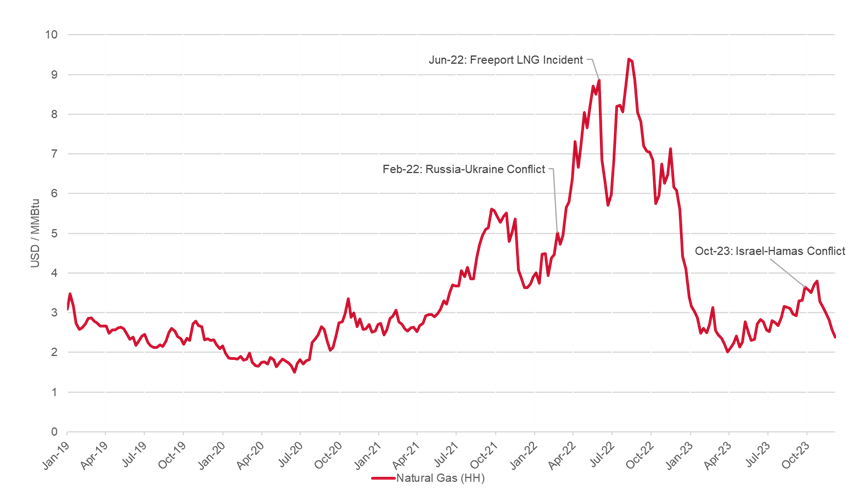

In recent years, natural gas prices were on a downward trend prior to the pandemic and the trend continued with a further decline due to the pullback in economic activity in 2020. We then saw the strong recovery of the global economy and prices increased well above the pre-pandemic level in 2021.

This briefing will highlight three recent significant events in the natural gas market: the Russia-Ukraine conflict in February 2022, the Freeport LNG incident in June 2022 and the Israel-Hamas conflict in October 2023.

Russia-Ukraine Conflict

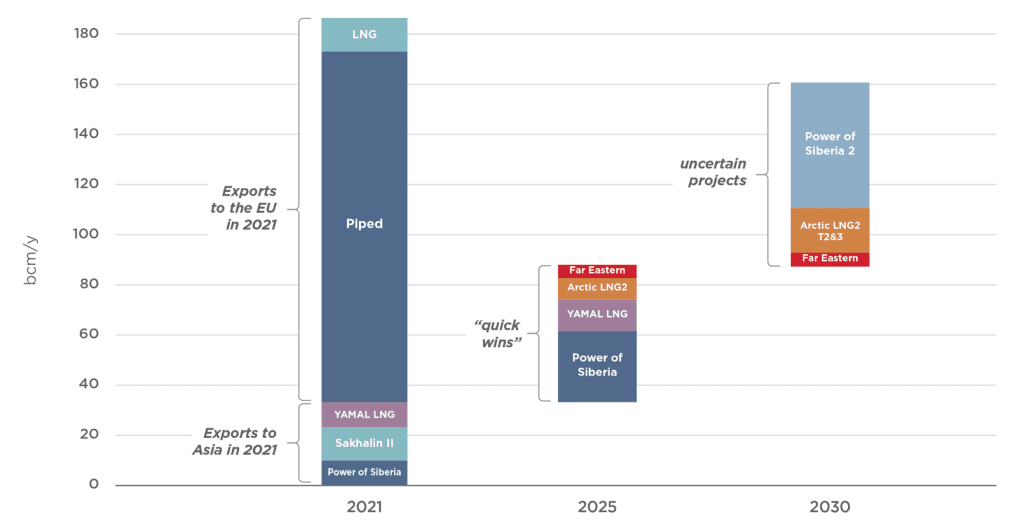

Just prior to the conflict, the EU’s reliance on natural gas imports from Russia was substantial, accounting for approximately 40%. Similarly, Russia exported most of its natural gas to the EU, demonstrating a mutual economic reliance between the two regions at the time.

To achieve quick wins by 2025, Russia aims to divert more LNG to Asia and to increase gas supply to China via the existing Power of Siberia pipeline. Russia recently announced a new daily record in gas pipeline exports to China, and the total gas export in 2023 was nearly 1.5 times higher than shipments in 2022, slightly exceeding contractual obligations. Projected capacity by 2025 is anticipated to be almost five-fold compared to the export volumes of 2023.

There are a few uncertain projects currently ‘in the pipeline’, the main one being the Power of Siberia 2 pipeline, which would establish gas connections between Western Russia (previously designated for European export) and China. While the two countries are finalising agreements, no supply contract has been signed yet. In the best-case scenario, the Power of Siberia 2 might commence operation after 2030 as the construction would require at least 5 years. This pipeline has the potential to position China as Russia’s main gas importer.

Nonetheless, even with multiple projects scheduled to be operational by 2030, it appears unlikely that Russian gas supplies to Asia will match the levels supplied to the EU during 2021.

Global conflicts and NZE initiatives have had a significant impact and will continue to have a future impact on natural gas and liquified natural gas (LNG) markets, which likely will be the last fossil fuel to be phased out to meet NZE goals. In response to the conflict in Ukraine, the EU is managing the demand for natural gas usage and, at least in the short term, has decreased natural gas consumption by 18% from August 2022 to March 2023, compared with the same period in recent years.

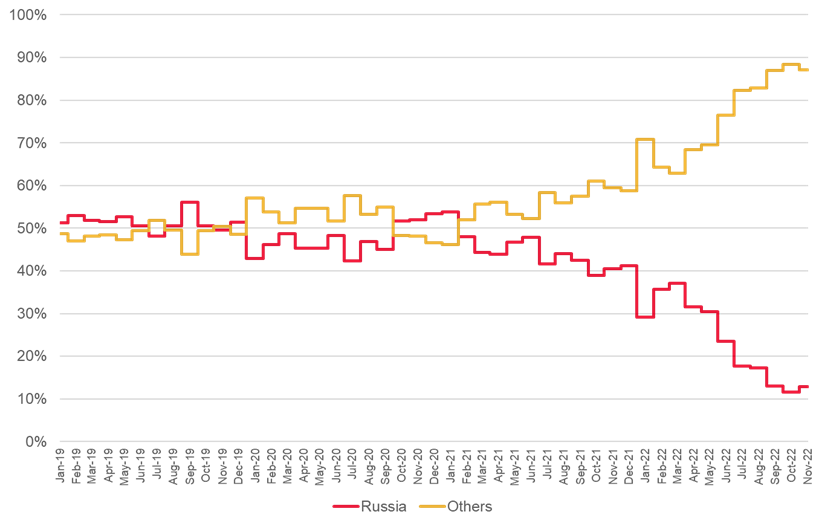

Europe has also drastically reduced gas imports from Russia that were received via pipeline, from the pre-invasion rate of 50% to about 10% in 2022, as shown below.

Our research shows that the EU import of natural gas from Russia has dropped a further 50% in 2023, so the total natural gas received from Russia is now only about 5%. Of interest, the EU has not changed the amount of LNG it receives from Russia, although it represents a small percentage of total gas demand. Whilst the EU has increased imports of natural gas from other pipelines in the North and Caspean Sea, as well as Eastern Europe, it has not been enough to replace the gas previously provided by Russia.

The EU has turned to LNG imports to fulfil the remaining demand for gas, mainly from the US. There has been a notable shift in the market, with an increasing volume of Russian gas being directed towards China, which results in a decrease in LNG imports in Asia and a substantial increase in LNG supply flowing towards the EU instead.

LNG is in a liquid-like state, which takes up only 1/600th of the original gas volume. However, there is a significant capital cost involved to produce and transport LNG, to store it and for its regasification at the receiving terminals. The various cost components of LNG are listed below.

- 11% exploration and production;

- 42% refrigeration and liquefaction;

- 20% transportation; and

- 27% storage and regasification

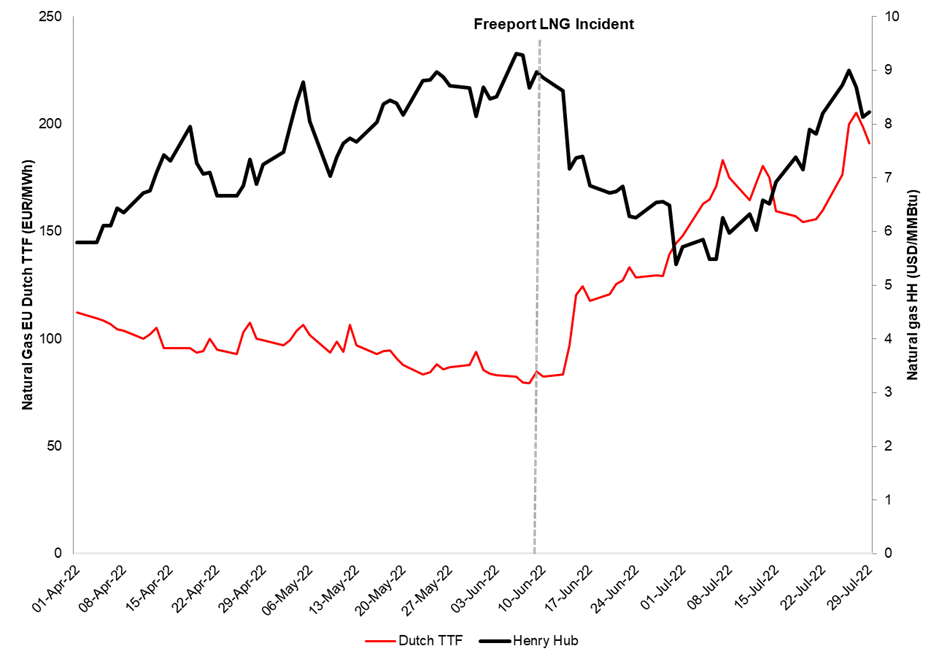

As noted above, following the Russia-Ukraine conflict, the EU’s gas balance has shifted from the Russian pipeline to global LNG supplies, mainly from the US. However, the situation got more complicated with the Freeport LNG incident in June 2022.

Freeport LNG Incident

The Freeport LNG export facility, handling 15 million tonnes per annum (around 20% of U.S. LNG exports), is one of the largest in the world and the second largest in the United States.

Significant disruption occurred on June 8, 2022, when an explosion affected the Freeport LNG liquefaction plant in Texas. With Freeport LNG exports being suspended from June 2022 to February 2023, this marked a pivotal moment in the history of US natural gas exports that showcased the deepening connection between US gas supply and global gas markets.

The timing of the shutdown coincided with a period of heightened global demand for LNG as many nations sought alternatives to reduce their reliance on Russian gas. With U.S. LNG exports experiencing a notable surge, a significant portion of Freeport LNG’s exports were directed towards Europe.

The aftermath of the incident had far-reaching consequences, contributing to a surge in LNG prices due to a supply shortage in the market. Conversely, the incident had a profound impact on U.S. LNG exports, leading to a redirection of more natural gas into storage. The resulting surplus of natural gas in the U.S. market caused a decline in domestic natural gas prices, as the Freeport LNG terminal, a major gas buyer, ceased its purchasing activities.

Israel-Hamas conflict

While the global energy market was still readjusting to the aftermath of the Russian-Ukraine conflict, an escalation in geopolitical tensions in the Middle East has kept the markets on edge since 7 October 2023.

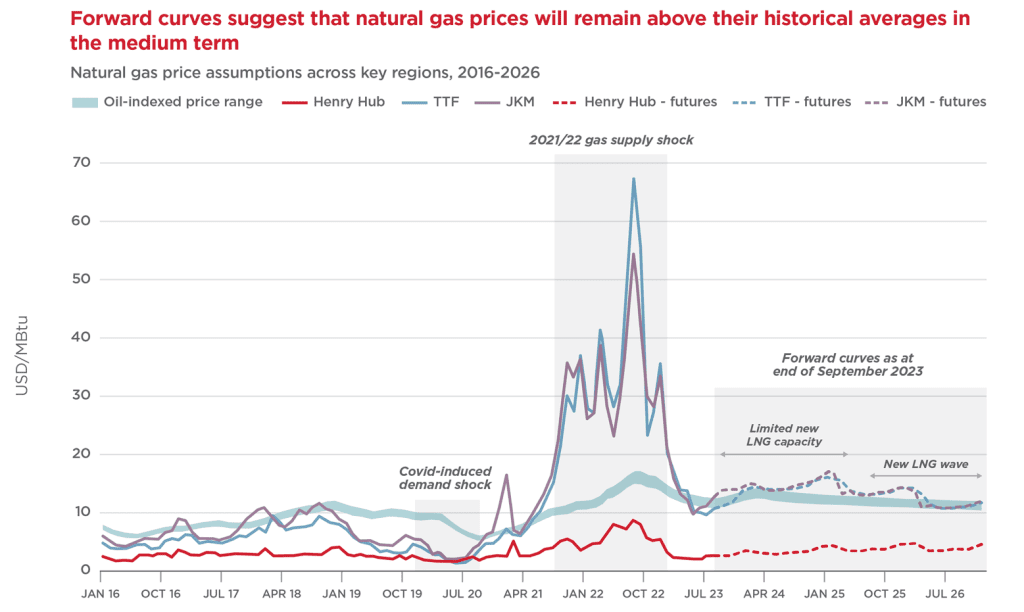

As the escalation of the conflict raised safety concerns, Israel shut down the production at its giant Tamar gas field off its southern coast. European natural gas prices rose more than 50% in a month, hitting an eight-month high of €56 per megawatt-hour, amid concerns that a wider conflict in the Middle East could disrupt gas supplies. However, the impact on gas markets was limited and temporary. After a large spike, the prices retreated and reached pre-conflict levels, as can be seen in the chart below.

Global events such as these show how volatile prices can become in a very short time period. With such price volatility, forecasting prices becomes challenging, making it difficult to set loss reserves accurately from the outset. Also, sums insured which are often set months before policy inception might be understated or overstated due to this fluctuation.

According to the International Energy Agency (IEA), forward-looking projections of gas prices are expected to remain fairly stable into the mid-term future and show a stabilisation through 2026 as a new wave of LNG liquification and regasification plants are planned to come online beginning in 2025. It’s important to note that projections inherently carry uncertainty, as the future is unpredictable. This projection was formulated before July 2023 and did not account for events such as the Israel-Hamas conflict in October 2023. We shall wait and see how gas prices evolve in the future.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

Graph 1 – https://www.bbc.com/news/science-environment-68110310

Graph 4 – https://www.tradingeconomics.com

Graph 5 – https://globallnghub.com/how-quickly-can-russia-divert-its-gas-supplies-from-europe-to-asia.html

Graph 6 – https://www.consilium.europa.eu/en/infographics/eu-gas-supply/

Graph 7 – https://www.tradingeconomics.com

Graph 8 – https://www.tradingeconomics.com

Nattakarn Prasitsumrit

ACMA, CGMA, CFE, CVA, Senior Manager

- +65 6327 3785

- nprasitsumrit@mdd.com

- Singapore, APAC

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Oil, Inflation, and the Dollar: The Global Impact of the Hormuz Crisis

The recent escalation involving Iran has once again drawn global attention to the Strait of Hormuz. This narrow stretch of water plays a critical role in the modern energy system, linking the Persian Gulf to the open ocean via the...

Floatovoltaics – Where Sun Meets Water

Renewable energy has been a source of energy for thousands of years and has been successfully utilized by humans. Most common sources of renewable energy include, but are not limited to, solar, wind, hydro, etc. with hydro energy being most...

Power Generation in the United States – Current Situation

Much has been said in recent times about the ever-increasing need for greater energy supply to meet the growing demand from power-hungry technologies like data centers, artificial intelligence (AI) and electric vehicles (EVs). But how are we faring in the...

Transforming the Petrochemical Landscape

The global energy industry is undergoing a dramatic shift as traditional refining processes evolve to meet the burgeoning demand for petrochemicals while contending with price volatility and environmental mandates. Navigating Global Energy Market Fluctuations The energy sector is no stranger...

Transitioning to Sustainable Power Generation: A Global Perspective

In recent years, the transition to renewable energy has become a central focus for nations across the globe. This movement is driven by the urgent need to address climate change, reduce carbon emissions, and meet the growing energy demands of...

Examining Volatility in the Energy Markets

Introduction In this technical briefing, we aim to provide an update on key Oil and Gas market indices and discuss whether we have moved past the significant volatility experienced between 2020 and 2024, or if the uncertainties persist in the...

Deep-Sea Mining – Panacea or Problem?

For quite some time now, much has been said about the world’s move toward clean energy and the goal toward net zero by 2050. To achieve this, demand will continue to grow for certain critical minerals, such as lithium, nickel,...

How is Electrification Disrupting the Energy Sector?

One of the biggest trends shaping society today is the widespread adoption of Electric Vehicles (EVs). While Tesla pioneered this movement as a disruptor, nearly every automobile manufacturer worldwide is now actively developing its own electric vehicles. Governments have implemented...

Carbon Capture – Is it Really Going to Materialise?

Before we discuss the carbon capture process and how it is used, it is worthwhile conceptualising the carbon emissions emitted worldwide and why different technologies, including carbon capture, must be considered as part of the energy transition. As can be...

Natural Gas – The Past, Present and Future

There has been a significant push towards transitioning to cleaner and renewable energy sources, moving away from fossil fuels due to their environmental impact. By looking at the past, the present and the future, the question remains: can we realistically...

Renewable Energy Losses – Winds of Change

It is May 20, 1899. New York City taxicab driver Jacob German is the recipient of the United States’ first-ever speeding ticket. He whizzed by at 12 miles per hour on Lexington Avenue and was then pursued and remanded by...

Losses")

Biomass (Co-Generation) Losses

Certain agricultural entities can generate energy from the organic matter derived from their production process. This type of co-generation of energy is referred to as biomass energy. These biomasses can be agricultural in nature, as in the case of sugarcane...

Variable Mining Costs – How Should They Be Treated?

Variable expenses: one would consider this to be one of the easier aspects in the analysis of a mining claim; however, that is far from the truth. When it comes to mining losses, the determination of which costs are considered...

The Effect of Volatility on Power Generation Business Interruption Losses

It is clear to the casual observer that many aspects of the economy are facing volatility. Fuel, energy, labor, shipping - all have experienced unprecedented shortages and price increases because of a myriad of conditions. The Russia-Ukraine war, Covid-19, inflation,...

Upstream Oil and Gas Losses

In this briefing, we discuss various considerations in upstream oil and gas production losses, and in particular how rates of production depend on the type of well. We also discuss what the shift to horizontal drilling and hydraulic fracturing means...

How is the Power Generation Landscape In Canada Evolving and What Are The Challenges It Faces in the Near Future?

Canada is a world leader in power generation as it pertains to sources that do not emit greenhouse gasses. At the current moment, 83% of generation comes from non-emitting sources. Canada’s goal by 2030 is to have 90% of power...

Back to Coal mining in the UK, what about the risk, which risk?

If you have an interest in energy, heavy industry or simply ESG you cannot fail to have seen the news towards the end of last year - that the UK has approved its first coal mine for many years. The...

Waste to Energy

What is Waste to Energy? Waste to energy refers to the process of converting municipal solid waste (MSW), otherwise known as trash, into usable heat, electricity, or fuel. The three main MSW categories include: Biomass or biogenic (plant or animal...

An Introduction to Natural Gas: Separation, LNG and GTL Plants

Our first technical briefing introduced the Oil & Gas value chain, divided into: i) upstream; ii) midstream; and iii) downstream. Here is a recap, before we explore natural gas in more detail. Upstream: this involves the exploration and extraction of...

Imbalance of Gas Supply

The sanctions imposed on Russia amid the Russia-Ukraine conflict have impacted global gas markets, particularly those in Europe. Russia is the second largest producer of natural gas globally and used to supply about 40% of Europe's natural gas. However, supplies...

Renewable Energy Certificates

Since 1978, American regulators and policymakers have looked to incentivize the investment and development of generating renewable energy. Individual states began enacting Renewable Portfolio Standards (RPS) to support this mission by requiring a specific percentage of a utility’s energy portfolio...

Potential Quantification Issues for Losses Involving Wind Farms Under Construction

Quantifying the financial impact stemming from the failure of an already commissioned single stand-alone wind turbine generator presents challenges, but these challenges increase exponentially when the failure occurs at a wind farm under construction. Additional complexities surface to the extent...

The Global Energy Crisis

As the Ukrainian conflict unfolds, Europe’s energy dependence on Russia becomes an increasingly critical bargaining tool. The economic sanctions imposed by some Western nations in response to Russia’s invasion appear to be increasingly directed against Russian oil and gas supplies...

Measuring Refining Margins for a BI Loss

When it comes to Business Interruption policies for Oil & Gas risks, there are different types of coverage available in the market, including Gross Profit, Gross Earnings, Specified Standing Charges etc. Common Policy Wordings Gross Profit equates to Turnover less...

in Refinery Claims")

The Importance of Linear Programs (LPs) in Refinery Claims

The use of Linear Program models is common in refining, and other industries, to optimise their activities by using an algorithm subject to a set of inputs, constraints, and relationships. This article discusses the LP models in more detail and...

What Happened to Jet Fuel During Covid-19?

The main types of jet fuels used by airlines are Jet A-1, Jet A and Jet B. Jet A is mainly used in the United States, whereas Jet A-1 is commonly used outside the United States and Jet B is...

The Recovery of Oil & Gas: A Roller Coaster Ride or Merely a Few Speed Bumps?

Covid-19 has led to major disruptions across various sectors and the petroleum industry is no exception. Demand for oil and petroleum products, in general, declined due to reduced economic activity as governments worldwide imposed lockdowns and tightened border controls. Certain...

What Triggered the UK Energy Market Crisis and What is the Impact on BI Claims?

The UK’s energy wholesale markets have reached new highs, with daily average electricity prices rising above GBP 150 per MWh since early September 2021. A record high of GBP 424 per MWh, since at least January 2019, was reached on...

Introduction to the Oil & Gas Value Chain

The Oil and Gas industry in the insurance market is usually categorised between Onshore/Offshore or Upstream/Downstream. It includes a chain of businesses relating to extraction, transportation, refining, petrochemical and chemical – essentially from the carbon in the ground to the...

The Effect of Deductibles & Policy Wording – Is It What You Think?

With a typical Energy claim standing at approximately USD 4.5 million, it’s no surprise that Business Interruption (BI) is once again the #1 business risk for the fourth year in a row[i]. To help insurers mitigate their exposure when an...

Court Breaks with Apportionment

The case of Varco Canada Limited v. Pason Systems Corp., 2013 FC 750 (CanLII) involved an award of over $52M based on an accounting of the defendant’s profits. Perhaps more importantly, the decision sheds light on a number of conceptual...