The Global Energy Crisis

11 March, 2022

11 March, 2022-

Katharina Wilson, Phillip Taylor

Katharina Wilson, Phillip Taylor

As the Ukrainian conflict unfolds, Europe’s energy dependence on Russia becomes an increasingly critical bargaining tool. The economic sanctions imposed by some Western nations in response to Russia’s invasion appear to be increasingly directed against Russian oil and gas supplies and could result in severe consequences for the global energy market. The humanitarian cost of these tragic events is incomprehensible, and the shift in the global energy supply could potentially impact the livelihoods and finances of consumers, small and large businesses, as well as the oil and gas industry in both the East and the West via a complex interplay of supply and demand.

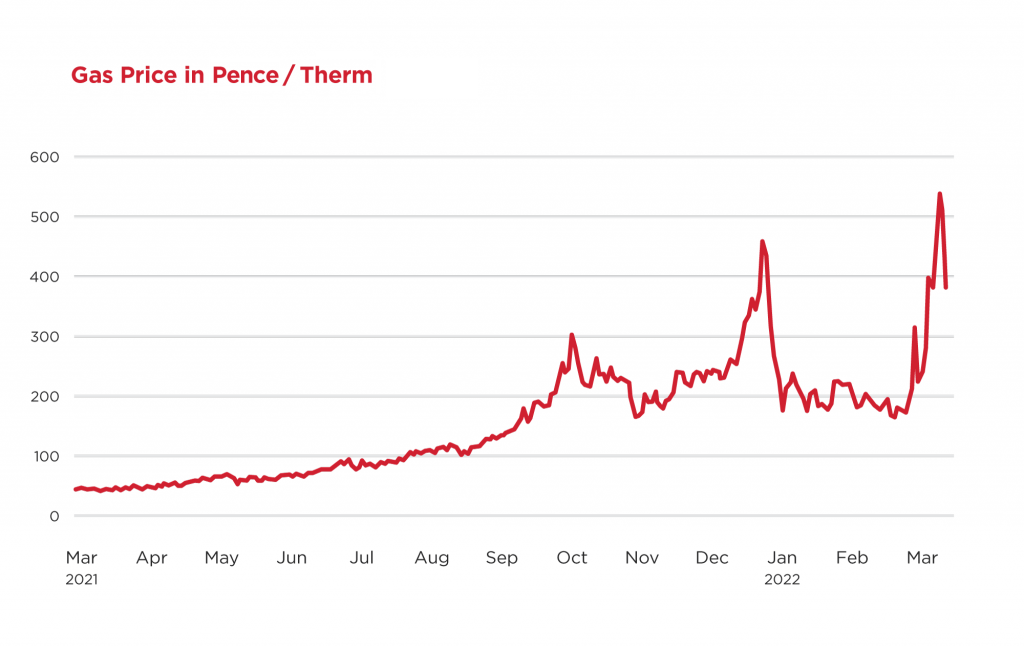

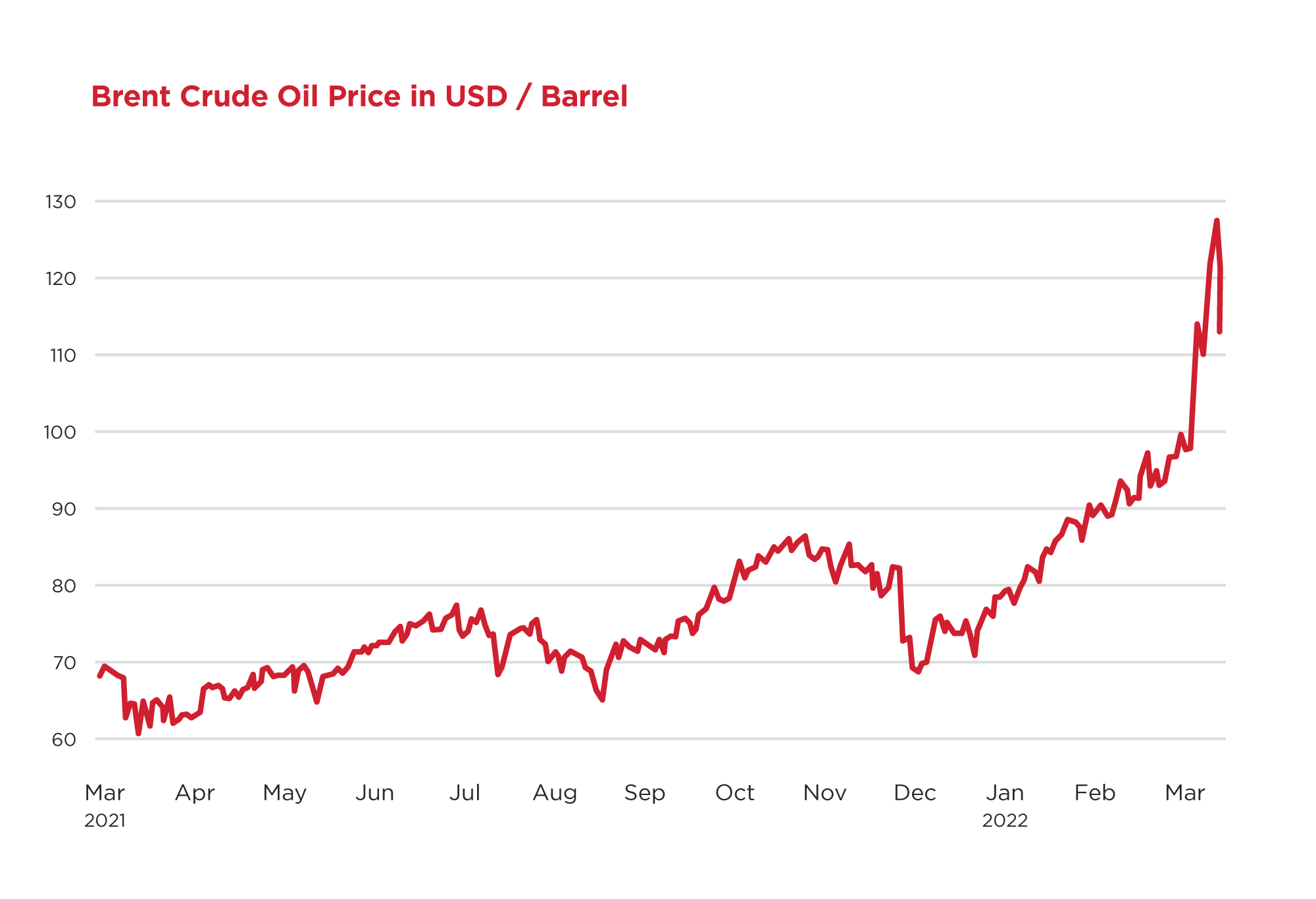

In response to the West’s increasing rejection of its oil, Russia threatens to disrupt the gas supply to Europe. Against the backdrop of heightened economic activity following the pandemic, low gas storage levels and high carbon prices, the world has already faced an energy crisis with soaring prices. In early March 2022, natural gas prices reached record heights of more than 500 pence per therm compared to prices of around 180 pence per therm one month earlier and 45 pence per therm one year ago [1]. Likewise, oil prices were soaring above USD 120 per barrel compared to USD 92 per barrel one month ago and prices of between USD 60 and USD 70 per barrel in March 2021 [2].

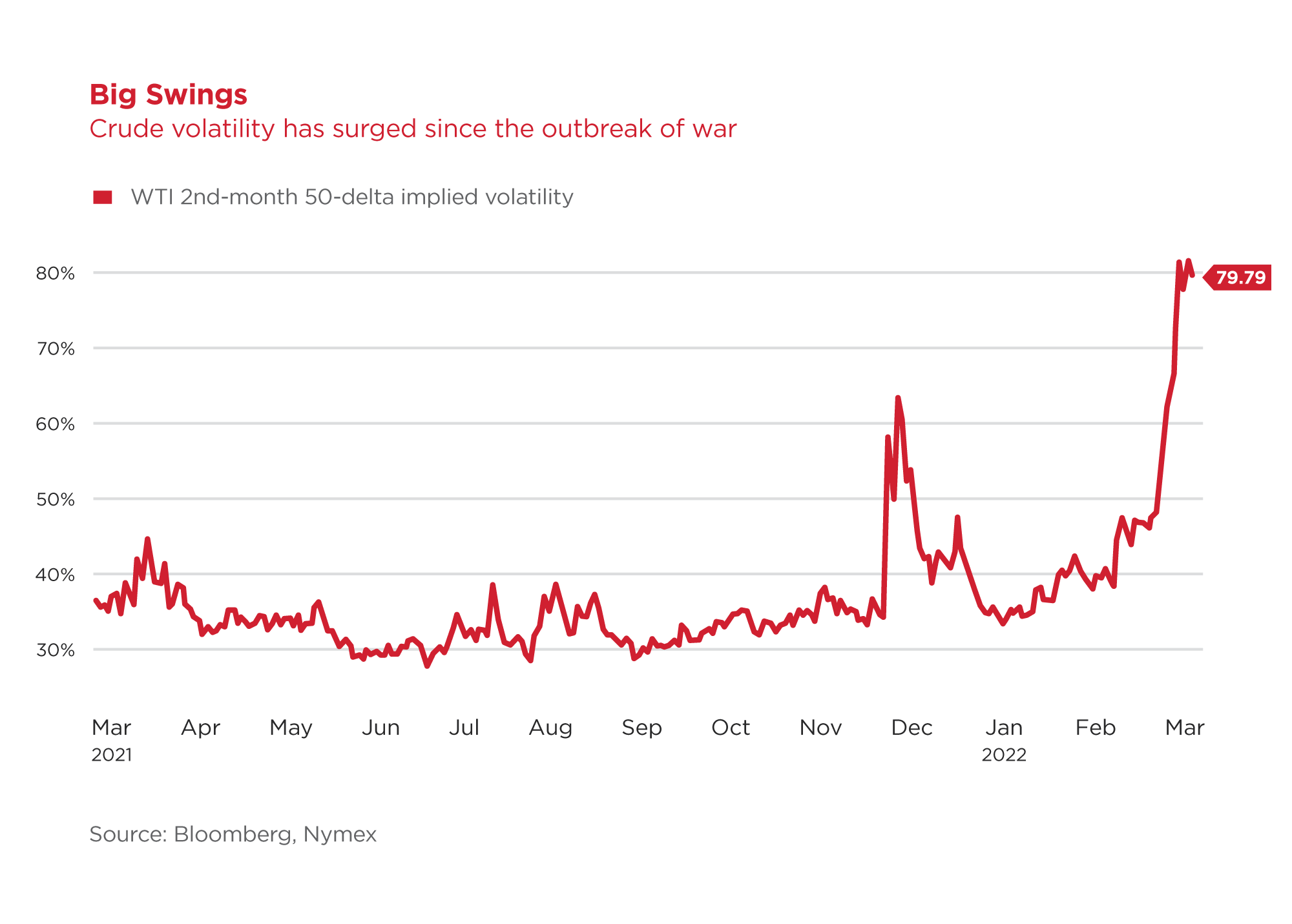

The impact of geopolitical decisions is significant volatility in oil and gas prices. On 9th March alone, the oil price rose to over USD 130 per barrel, only to close at around USD 105 per barrel, following news that the UAE called for OPEC members to increase output. The chart below shows how volatile the crude market has become in recent weeks.

This volatility arises because Russian oil and gas represent a significant proportion of supply to Europe and Asia Pacific countries and the removal of that supply leads to an imbalance in the supply and demand for these fuels.

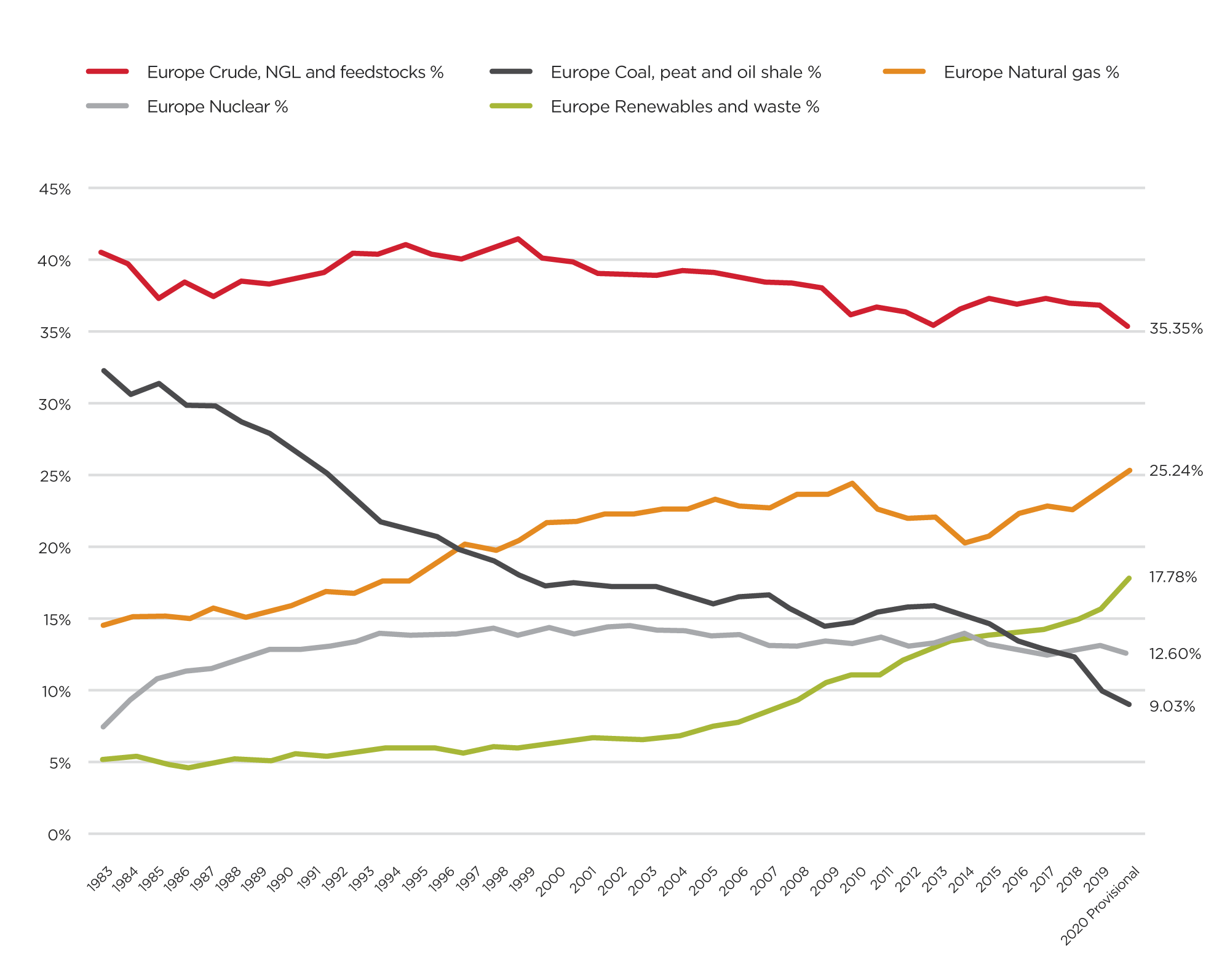

In the last two decades, Europe has driven a global focus on reducing greenhouse emissions and the shift from carbon-intense coal towards gas and green energy supply, as demonstrated in the below graph [3]:

Around 40% of the EU’s gas supply is imported from Russia, mainly via the Yamal, Ukraine Transit and Nord Stream 1 pipelines [4]. This interdependency would deepen under Germany’s original pre-crisis plan to double its gas imports via the planned Nord Stream 2 pipeline. In 2020, Russia exported 72% of its natural gas to OECD Europe, of which Germany (16%), Italy (12%) and France (8%) were the biggest recipients [5]. The remainder of Russian gas exports went to Asia and Oceania (11%) and non-OECD Europe and Eurasia (17%).

Russia is the third-largest producer of crude oil, after the USA and Saudi Arabia, exporting more than 40% of its production in 2021, with the distribution being around 50-60% to Europe and about 40% to Asia Pacific countries (mainly China).

Replacing Russian oil and gas is not an easy task, but the European Commission recently responded with its REPowerEU plan to end the reliance on Russian energy by 2030. The program entails increased gas imports from Norway, the UK and the Netherlands and more LNG imports from the US and other suppliers. At the same time, the shift towards green energy is likely to accelerate in Europe with a ramp-up of renewables, biogas and hydrogen. The plan would also entail increased use of coal in some nations while the alternatives are being established. This would allow Europe to end its dependency on Russian oil and gas and reduce CO2 emissions in the long run. In the short run, however, carbon emissions may rise, leading to higher CO2 emissions and potentially higher costs associated with the EU’s and UK’s Emissions Trading Schemes. Volatile oil, gas, electricity, and emission prices directly impact the margins of European and global energy producers as well as various other industries.

What does this mean for business interruption claims? The effects of the energy crisis and the ever-changing developments in fuel supply on future claims would require detailed analysis. When it comes to refineries and petrochemical plants, price volatility can certainly lead to volatility in margins, but higher prices do not always lead to higher margins and vice-versa. Stay tuned for our next technical briefing which will discuss refining and petrochemical margins for business interruption losses in greater depth.

By Kat Wilson and Phillip Taylor.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

Phillip Taylor

FCMA, CGMA, CFE, Chief Operating Officer – EMEA & APAC

- ptaylor@mdd.com

- Singapore, APAC

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Oil, Inflation, and the Dollar: The Global Impact of the Hormuz Crisis

The recent escalation involving Iran has once again drawn global attention to the Strait of Hormuz. This narrow stretch of water plays a critical role in the modern energy system, linking the Persian Gulf to the open ocean via the...

Floatovoltaics – Where Sun Meets Water

Renewable energy has been a source of energy for thousands of years and has been successfully utilized by humans. Most common sources of renewable energy include, but are not limited to, solar, wind, hydro, etc. with hydro energy being most...

Power Generation in the United States – Current Situation

Much has been said in recent times about the ever-increasing need for greater energy supply to meet the growing demand from power-hungry technologies like data centers, artificial intelligence (AI) and electric vehicles (EVs). But how are we faring in the...

Transforming the Petrochemical Landscape

The global energy industry is undergoing a dramatic shift as traditional refining processes evolve to meet the burgeoning demand for petrochemicals while contending with price volatility and environmental mandates. Navigating Global Energy Market Fluctuations The energy sector is no stranger...

Transitioning to Sustainable Power Generation: A Global Perspective

In recent years, the transition to renewable energy has become a central focus for nations across the globe. This movement is driven by the urgent need to address climate change, reduce carbon emissions, and meet the growing energy demands of...

Examining Volatility in the Energy Markets

Introduction In this technical briefing, we aim to provide an update on key Oil and Gas market indices and discuss whether we have moved past the significant volatility experienced between 2020 and 2024, or if the uncertainties persist in the...

How is Electrification Disrupting the Energy Sector?

One of the biggest trends shaping society today is the widespread adoption of Electric Vehicles (EVs). While Tesla pioneered this movement as a disruptor, nearly every automobile manufacturer worldwide is now actively developing its own electric vehicles. Governments have implemented...

Carbon Capture – Is it Really Going to Materialise?

Before we discuss the carbon capture process and how it is used, it is worthwhile conceptualising the carbon emissions emitted worldwide and why different technologies, including carbon capture, must be considered as part of the energy transition. As can be...

Natural Gas – The Past, Present and Future

There has been a significant push towards transitioning to cleaner and renewable energy sources, moving away from fossil fuels due to their environmental impact. By looking at the past, the present and the future, the question remains: can we realistically...

Renewable Energy Losses – Winds of Change

It is May 20, 1899. New York City taxicab driver Jacob German is the recipient of the United States’ first-ever speeding ticket. He whizzed by at 12 miles per hour on Lexington Avenue and was then pursued and remanded by...

Losses")

Biomass (Co-Generation) Losses

Certain agricultural entities can generate energy from the organic matter derived from their production process. This type of co-generation of energy is referred to as biomass energy. These biomasses can be agricultural in nature, as in the case of sugarcane...

The Effect of Volatility on Power Generation Business Interruption Losses

It is clear to the casual observer that many aspects of the economy are facing volatility. Fuel, energy, labor, shipping - all have experienced unprecedented shortages and price increases because of a myriad of conditions. The Russia-Ukraine war, Covid-19, inflation,...

Upstream Oil and Gas Losses

In this briefing, we discuss various considerations in upstream oil and gas production losses, and in particular how rates of production depend on the type of well. We also discuss what the shift to horizontal drilling and hydraulic fracturing means...

How is the Power Generation Landscape In Canada Evolving and What Are The Challenges It Faces in the Near Future?

Canada is a world leader in power generation as it pertains to sources that do not emit greenhouse gasses. At the current moment, 83% of generation comes from non-emitting sources. Canada’s goal by 2030 is to have 90% of power...

Waste to Energy

What is Waste to Energy? Waste to energy refers to the process of converting municipal solid waste (MSW), otherwise known as trash, into usable heat, electricity, or fuel. The three main MSW categories include: Biomass or biogenic (plant or animal...

An Introduction to Natural Gas: Separation, LNG and GTL Plants

Our first technical briefing introduced the Oil & Gas value chain, divided into: i) upstream; ii) midstream; and iii) downstream. Here is a recap, before we explore natural gas in more detail. Upstream: this involves the exploration and extraction of...

Imbalance of Gas Supply

The sanctions imposed on Russia amid the Russia-Ukraine conflict have impacted global gas markets, particularly those in Europe. Russia is the second largest producer of natural gas globally and used to supply about 40% of Europe's natural gas. However, supplies...

Renewable Energy Certificates

Since 1978, American regulators and policymakers have looked to incentivize the investment and development of generating renewable energy. Individual states began enacting Renewable Portfolio Standards (RPS) to support this mission by requiring a specific percentage of a utility’s energy portfolio...

Potential Quantification Issues for Losses Involving Wind Farms Under Construction

Quantifying the financial impact stemming from the failure of an already commissioned single stand-alone wind turbine generator presents challenges, but these challenges increase exponentially when the failure occurs at a wind farm under construction. Additional complexities surface to the extent...

The Global Energy Crisis

As the Ukrainian conflict unfolds, Europe’s energy dependence on Russia becomes an increasingly critical bargaining tool. The economic sanctions imposed by some Western nations in response to Russia’s invasion appear to be increasingly directed against Russian oil and gas supplies...

Measuring Refining Margins for a BI Loss

When it comes to Business Interruption policies for Oil & Gas risks, there are different types of coverage available in the market, including Gross Profit, Gross Earnings, Specified Standing Charges etc. Common Policy Wordings Gross Profit equates to Turnover less...

in Refinery Claims")

The Importance of Linear Programs (LPs) in Refinery Claims

The use of Linear Program models is common in refining, and other industries, to optimise their activities by using an algorithm subject to a set of inputs, constraints, and relationships. This article discusses the LP models in more detail and...

What Happened to Jet Fuel During Covid-19?

The main types of jet fuels used by airlines are Jet A-1, Jet A and Jet B. Jet A is mainly used in the United States, whereas Jet A-1 is commonly used outside the United States and Jet B is...

A Lightning Fast Intro to Energy Market Basics

The summer has come to an end in Florida. Temperatures are still hot, and the afternoon thunderstorms are raging. So, when I open my electricity bill and gasp at the month’s cost, muttering some hopeless comments about how I should...

The Recovery of Oil & Gas: A Roller Coaster Ride or Merely a Few Speed Bumps?

Covid-19 has led to major disruptions across various sectors and the petroleum industry is no exception. Demand for oil and petroleum products, in general, declined due to reduced economic activity as governments worldwide imposed lockdowns and tightened border controls. Certain...

What Triggered the UK Energy Market Crisis and What is the Impact on BI Claims?

The UK’s energy wholesale markets have reached new highs, with daily average electricity prices rising above GBP 150 per MWh since early September 2021. A record high of GBP 424 per MWh, since at least January 2019, was reached on...

Introduction to the Oil & Gas Value Chain

The Oil and Gas industry in the insurance market is usually categorised between Onshore/Offshore or Upstream/Downstream. It includes a chain of businesses relating to extraction, transportation, refining, petrochemical and chemical – essentially from the carbon in the ground to the...

Regulated and Deregulated Electricity Markets: What is the difference when modelling power generation losses?

Introduction When modelling power generation losses for Business Interruption (“BI”) or Delay in Start-Up (“DSU”) purposes, it is important to understand the type of market(s) the Insured participates in and specifically how it operates within those markets. In this introductory...

The Effect of Deductibles & Policy Wording – Is It What You Think?

With a typical Energy claim standing at approximately USD 4.5 million, it’s no surprise that Business Interruption (BI) is once again the #1 business risk for the fourth year in a row[i]. To help insurers mitigate their exposure when an...

Court Breaks with Apportionment

The case of Varco Canada Limited v. Pason Systems Corp., 2013 FC 750 (CanLII) involved an award of over $52M based on an accounting of the defendant’s profits. Perhaps more importantly, the decision sheds light on a number of conceptual...