Carbon Capture – Is it Really Going to Materialise?

10 May, 2024

10 May, 2024-

Edward Secchi

Edward Secchi -

EMEA

EMEA

Before we discuss the carbon capture process and how it is used, it is worthwhile conceptualising the carbon emissions emitted worldwide and why different technologies, including carbon capture, must be considered as part of the energy transition.

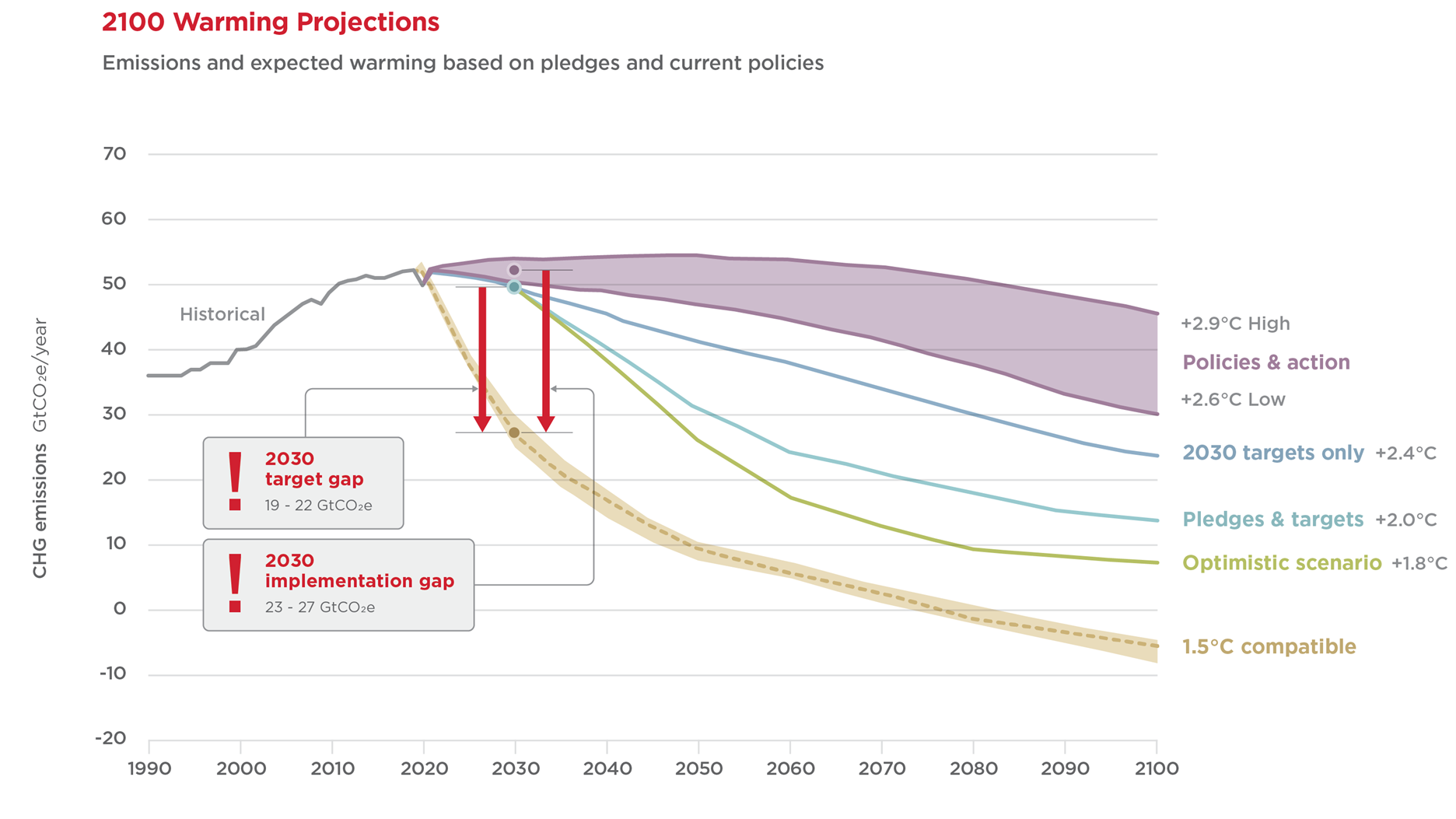

As can be seen from the chart below, emissions are increasing and continue to rise year-on-year, bringing us further away from the net zero scenario / 1.5°C target sought with energy transition.

Although government policies and actions are being established and implemented, these are expected to be a long way off driving down emissions to such a reduced level to be net zero / 1.5°C maximum compatible. In addition, most CO2 emissions are being released by industries we rely heavily on for everyday life, such as coal, oil and gas, with these three industries emitting about 90% of the world’s emissions.

So, let’s look at what is being done to try and reduce these emissions, specifically through carbon capture.

Carbon Capture Process

It is worth noting that CCS and CCU refer to capturing Carbon Dioxide (CO2) and either storing it permanently (CCS) or utilising it by converting it into valuable products, such as fuels and chemicals (CCU). The abbreviation to encapsulate both types of carbon capture technologies is CCUS (Carbon Capture, Utilisation and Storage).

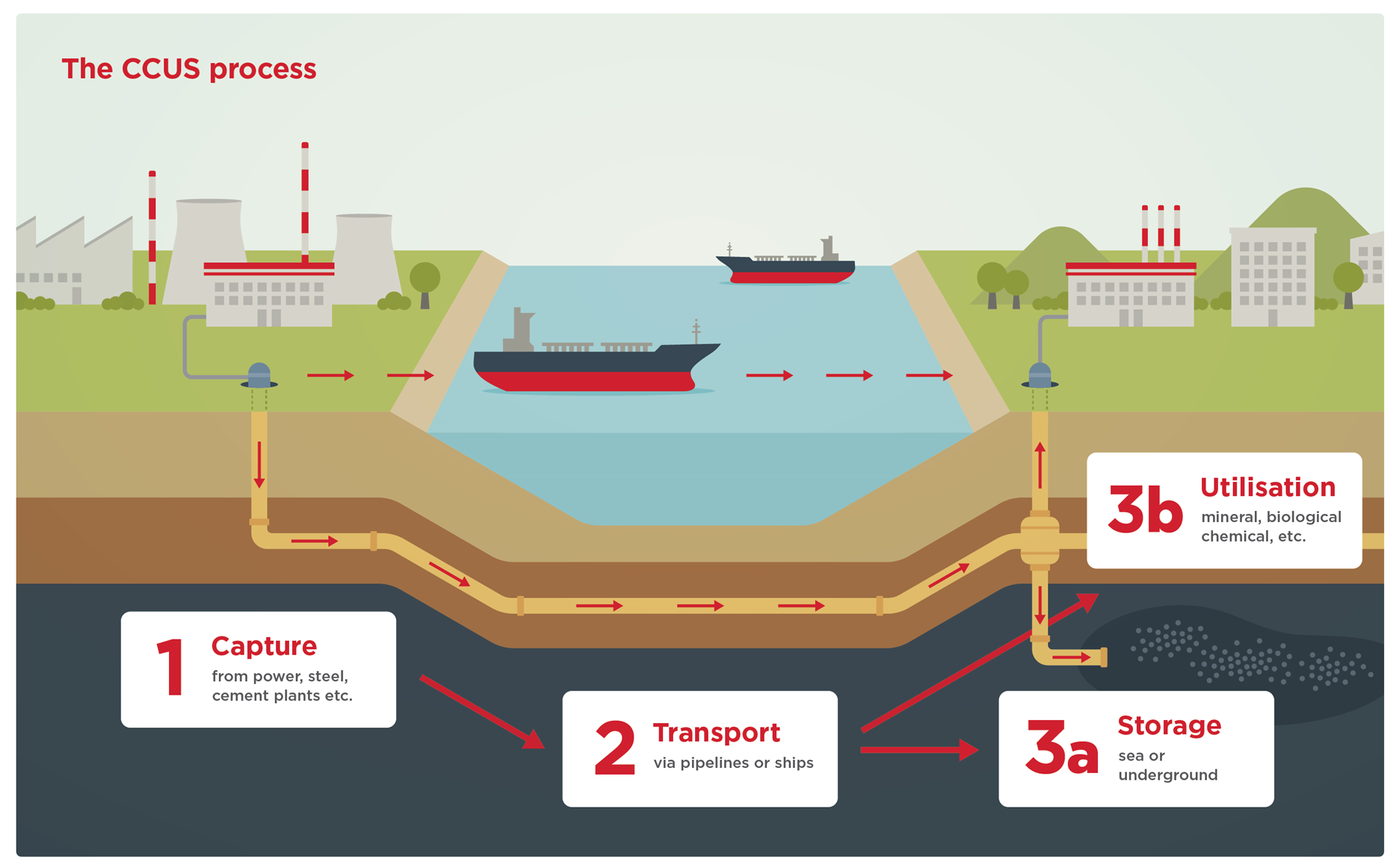

The high-level process involved in CCUS can be summarised as follows:

- Capturing carbon dioxide from large point sources like power generation or industrial facilities.

- Carbon dioxide is then compressed to transform it into a liquid-like state.

- This is then transported to a location where there are facilities to inject the CO2 deep underground. Typical storage sites for CO2 include saline aquifers or depleted oil and gas reservoirs, which typically need to be 0.62 miles (1km) or more underground.

- An alternative to the above is, rather than storing the CO2, it is reused / converted to building materials such as concrete and plastics via polymerisation or for enhanced oil recovery.

A summary of the process can be seen from the below image:

The process of capturing, condensing, transporting and then either storing or reusing the carbon is expensive due to the following:

- Capturing – The process of separating carbon dioxide (CO2) from other gases requires specialised and often energy-intensive technologies.

- Condensing – After capture, CO2 needs to be compressed or condensed into a liquid state for efficient transportation. This process also requires energy and specialised equipment.

- Transporting – Transporting CO2 to storage sites, often via pipelines or ships, adds to the cost and indeed the carbon footprint. The distance between the capture source and storage location can significantly impact costs.

- Storage: Securely storing CO2 underground in geological formations often involves drilling, monitoring, and long-term maintenance, all of which add to the overall costs.

Due to the above, one of the reasons that CCUS technology did not take off like more traditional renewable energy, as part of the energy transition, relates to cost.

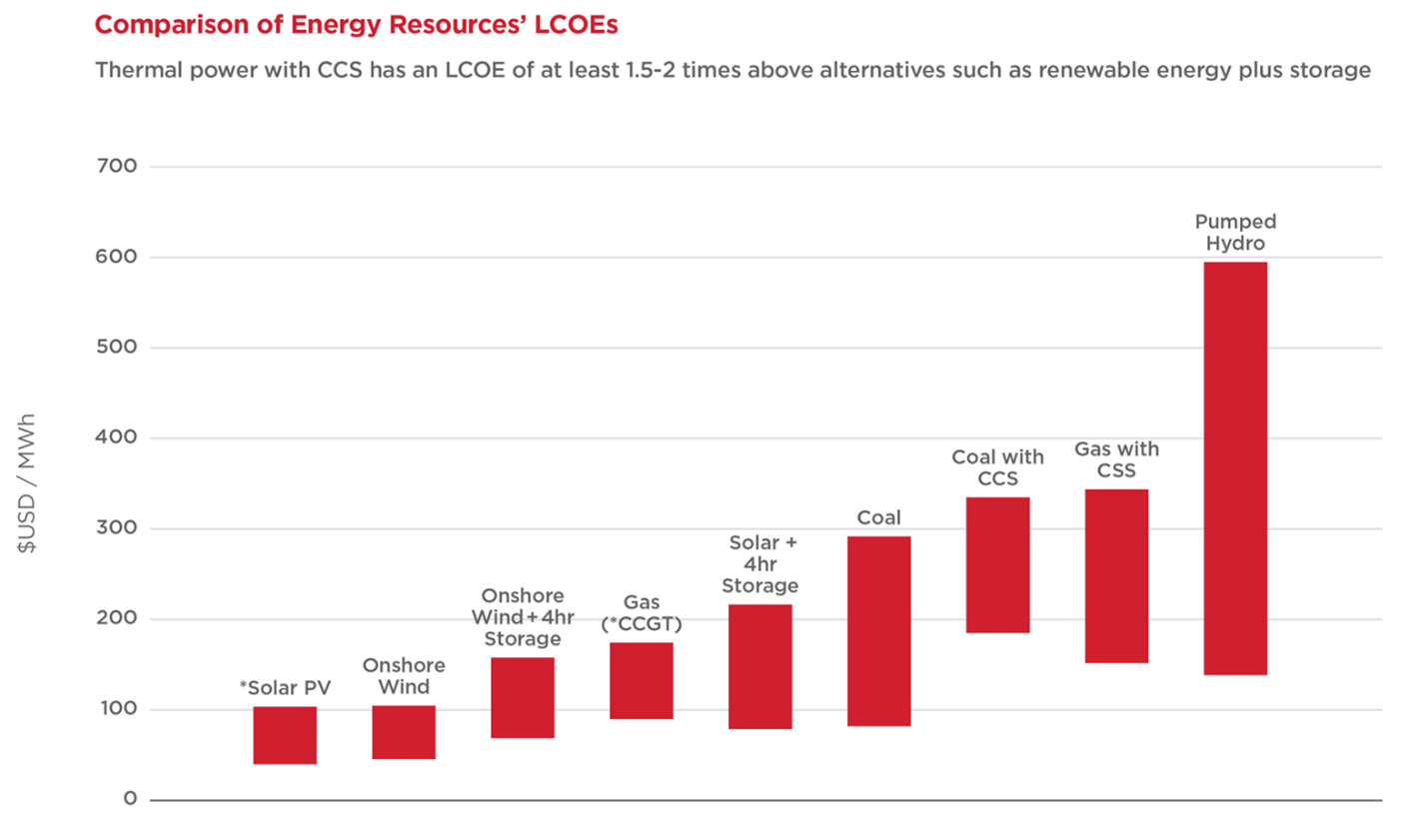

CCUS is more expensive than other more traditional renewable technologies. It is estimated that the Levelized Cost of Energy (LCOE), which represents an estimation of the cost of energy production, for thermal power with CCS technology is significantly more expensive than traditional renewable energy generation, as can be seen below:

An example of the cost implication to CCUS projects can be found in April 2023 when Norway temporarily halted a CCS project on a waste-to-energy plant due to high costs, with the project being permanently suspended shortly thereafter. While several other economic factors were at play (project cost overruns, geopolitical instability and its impact on energy prices, and a weakened Norwegian crown), it was decided that the funds would be better utilised elsewhere.

While LCOE costs may decrease over time, as CCUS becomes more advanced and new developments are made, in a similar way as we witnessed in the solar energy space, only time will tell if these materialise.

CCS Facilities

Notwithstanding the cost, the number of CCUS projects coming operational and being developed is growing. While CCUS is sometimes considered a new technology, the first CCS-related project started in 1972, using a waste stream of by-product CO2 from several natural gas processing facilities in the Val Verde area of southern Texas. Instead of being vented, the CO2 that had already been separated from the natural gas stream in the Val Verde gas plants was compressed and transported through the first large-scale, long-distance CO2 pipeline to an oilfield several hundred kilometres away elsewhere in Texas.

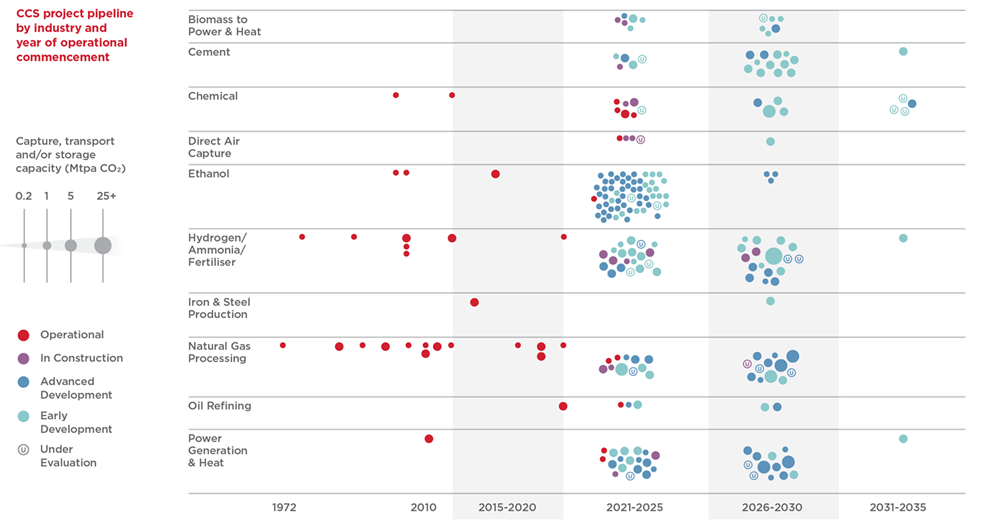

Since then, several other industries have adopted the technology, with a growing number of capture-at-source facilities being brought online or developed in recent years, as summarised below:

As can be seen from the above, there is a wide array of industries utilising carbon capture technology, with the number of projects being developed / considered increasing significantly from early 2021. As of 2021, the number of CCUS capture at source facilities were:

| Description | Americas | EMEA | Asia Pacific |

| # | # | # | |

| Operational | 20 | 6 | 10 |

| Construction | 6 | 6 | 8 |

| Advanced Development | 31 | 10 | 10 |

| Early Development | 20 | 30 | 15 |

A few examples of capture at source CCS facilities include:

- The Next Decade Rio Grande LNG facility is expected to capture about 90% of the emissions it emits to produce LNG. It should be noted however, that to get this project off the ground, the entity took advantage of 45Q tax credits, which made the capital and operating expenses, interest, transportation, and permanent storage reduce from an expected value of $70 / tonne of CO2 to approximately $17 / tonne.

- Petrobras in Brazil operates the first CO2 separation facility in Ultra Deep Waters, but to operate this project, they incur high monitoring costs to ensure that the carbon stays where it needs to be.

- In Saudi Arabia, a natural gas-to-liquid plant is expected to capture carbon from the atmosphere and inject it into a deep oil reservoir. This helps reduce emissions and utilise enhanced oil recovery processes to obtain more oil from the field.

- CCS Hub in Jubail, Saudi Arabia, is another initiative being developed where companies pool resources to use economies of scale. A CCUS hub takes carbon dioxide from several emitters and transports and stores it using common infrastructure. It reduces costs and risks for individual companies and governments and can open up CCUS as a decarbonisation option at scale.

- Pertamina Sukowati, Indonesia, will take CO2 and inject it to boost oil production through enhanced oil recovery mechanisms.

- PTTEP Thailand, a USD 300m facility, is expected to recover 1 million tonnes of CO2 per year when this plant becomes operational in 2026.

More recently, Climeworks’ “Mammoth” Direct Air Capture (DAC) plant in Iceland started operating on 8 May 2024. The main difference between CCS and DAC is that carbon capture focuses on capturing carbon dioxide emissions from industrial sources, while direct air capture targets atmospheric carbon dioxide. The “Mammoth” plant is expected to capture 36,000 tons of carbon from the atmosphere a year once operating at full capacity, which is equivalent to taking around 7,800 petrol-powered cars off the road for a year. However, Climeworks has stated that the cost of removing the carbon is around USD 1,000 / tonne, which is significantly more than the industry-estimated USD 100 / tonne threshold needed to make the technology affordable and viable.

Although the carbon captured at the plant is relatively limited and costly, as the plant increases in capacity and the technology becomes more advanced, Climeworks expects the cost to reduce to around USD 300 / tonne by 20230 and reach the USD 100 / tonne threshold by 2050. In the meantime, however, let’s consider what other entities are doing with emissions to make their capture more viable.

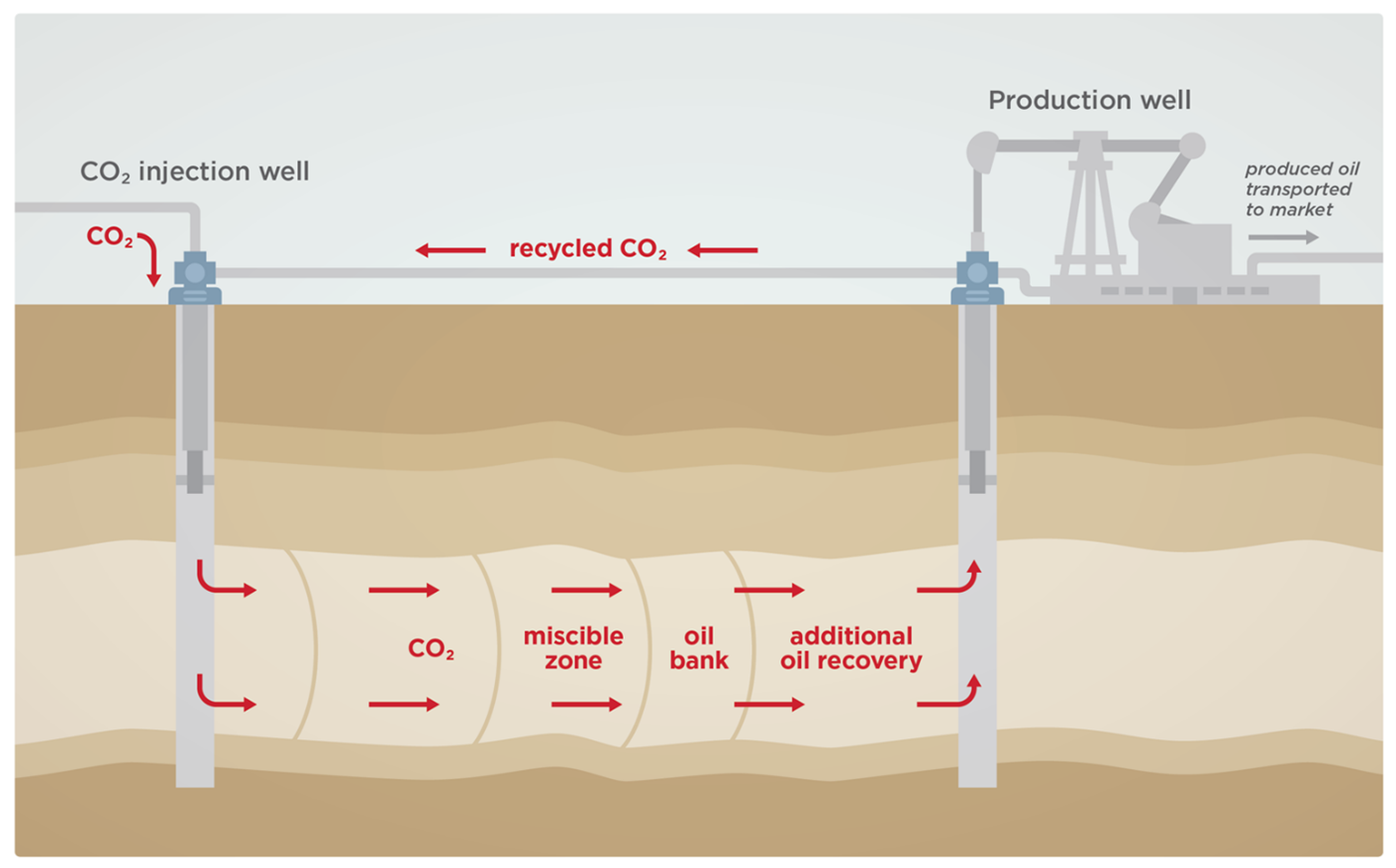

Enhanced Oil Recovery

As mentioned above, several projects are utilising CCUS technology to enhance their oil recovery, allowing them to be seen as “green” by reducing emissions but at the same time improving their bottom line.

CO2 enhanced oil recovery is a process of obtaining crude oil from the pores of rocks by injecting carbon dioxide into the subsurface to enhance oil recovery. During CO2 enhanced oil recovery, carbon dioxide mixes with oil, helping it move through the rock pore spaces which helps to recover more oil.

An overview of the EOR process is included below:

The above process can generally increase oil recovery from about 30-40%, using conventional means, to recover more than 60-80% of oil in the reservoir. To put the above into context, it is estimated that, of the total of 600 billion barrels of oil that have been discovered in the United States, approximately 400 billion barrels are unrecoverable by conventional methods. Half of that unrecoverable oil (200 billion barrels) is at reasonable depths at which EOR may be applicable.

Not Without Risks

Although there are arguments on whether CCUS, and especially the process of utilising CCUS for EOR purposes, is assisting to reduce emissions or is ultimately being used as a mechanism to safeguard the future of the fossil fuel industry through obtaining more fossil fuels, there are other risks associated with CCUS.

The captured CO2 is injected deep underground, and we must ensure it stays there. However, physical leakage from storage reservoirs is possible via gradual and long-term release or a sudden release of CO2 caused by disruption of the reservoir.

To conceptualise the above, we have included a few examples of CCS incidents / concerns below:

- California Aliso Canyon gas leak in 2015, the worst man-made greenhouse gas disaster in US history, when 97,000 tonnes of methane leaked into the atmosphere. While the leak at Aliso Canyon was a methane, not a carbon dioxide, leak, depleted oil and gas reservoirs are commonly used to store captured carbon dioxide and so the problems encountered at Aliso Canyon could also be encountered with carbon dioxide at carbon capture projects.

- In Salah, Algeria, a carbon capture project with a total cost of USD 2.7 billion. Injection started in 2004 and was suspended in 2011 due to concerns about the integrity of the seal and suspicious movements of the trapped carbon dioxide under the ground.

- Lake Nyos, Cameroon in 1986, around 1,700 people died after a release of carbon dioxide from the lake. It should be noted that this last example is not man-made, and the CO2 had built up under high pressure in Lake Nyos, which is a volcanic lake. However, it shows the impact of approximately 100-300k tonnes of carbon (relatively minor compared to some of the projects mentioned above) being released into the atmosphere.

Where Next

Notwithstanding the above concerns, we are seeing success stories revolving around CCUS.

The world’s first commercial-scale CO2-to-methanol plant started production in Anyang, Henan Province, China, in October 2023. The cutting-edge facility is the first of its type in the world to produce methanol — a valuable fuel and chemical feedstock. The facility is expected to capture 160,000 tonnes of carbon dioxide emissions a year, equivalent to taking more than 60,000 cars off the road, to produce 110,000 tonnes of methanol per year through Emissions-to-Liquid technology (ETL).

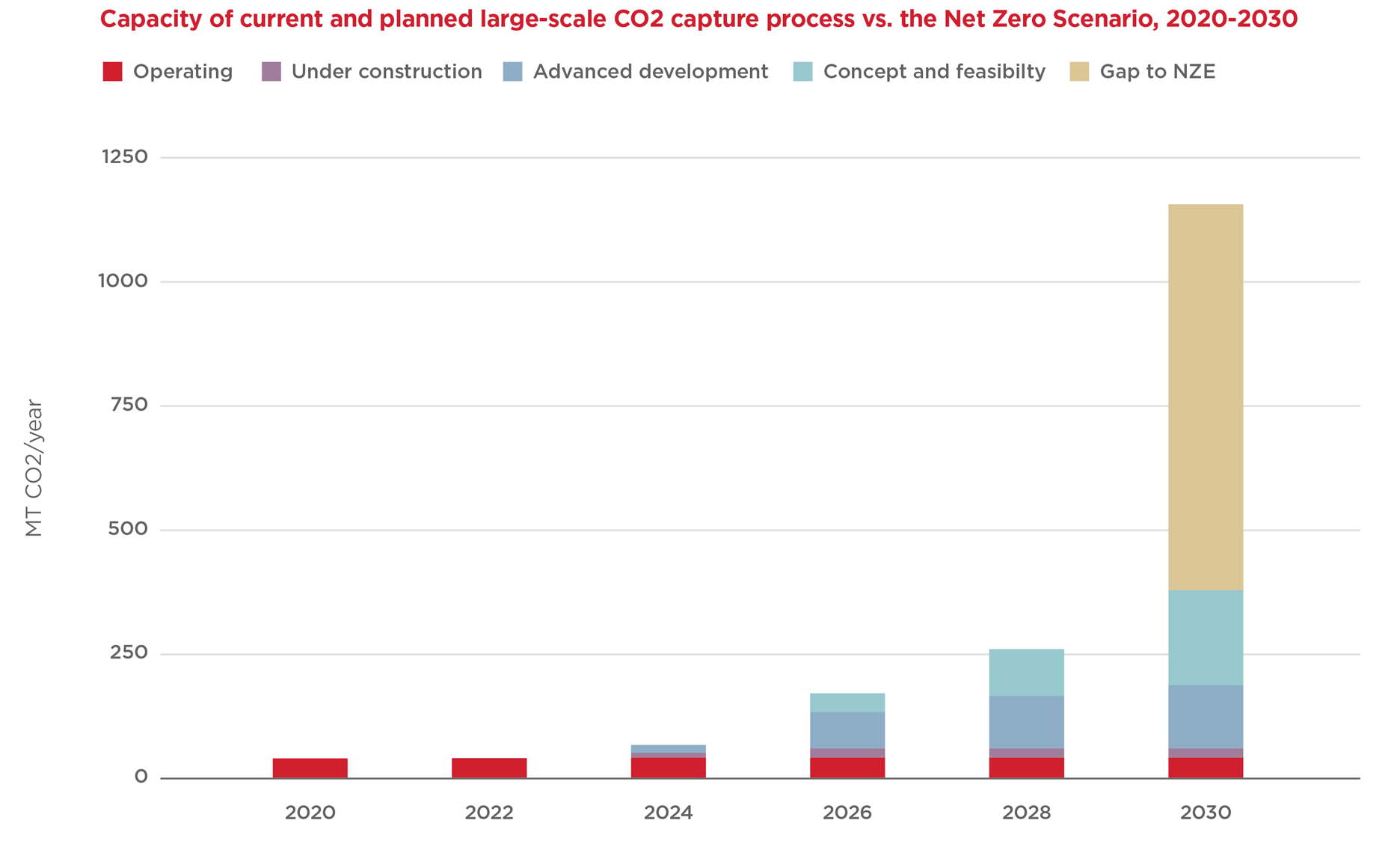

While CCUS is becoming more mainstream, with several industries developing facilities around the world, there is still a long way to go if this technology is to make a significant dent in reducing emissions.

Of the handful of products that are currently operational / in development, if net zero targets are to be achieved, it is estimated that another 1,000 large-scale [1] projects are needed as can be seen from the below IEA study.

To account for the potential growth of CCS projects, the Insurance market is developing new products. AON recently announced that it has developed a new insurance product for international transport and storage companies engaging in storing carbon dioxide. It will be interesting to see what this brings in terms of coverage offered, how values will be established and the quantification of claims should an incident occur.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

The Global CCS Institute (GCCSI) considers projects capturing over 1 Mtpa as large-scale

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Oil, Inflation, and the Dollar: The Global Impact of the Hormuz Crisis

The recent escalation involving Iran has once again drawn global attention to the Strait of Hormuz. This narrow stretch of water plays a critical role in the modern energy system, linking the Persian Gulf to the open ocean via the...

Floatovoltaics – Where Sun Meets Water

Renewable energy has been a source of energy for thousands of years and has been successfully utilized by humans. Most common sources of renewable energy include, but are not limited to, solar, wind, hydro, etc. with hydro energy being most...

Power Generation in the United States – Current Situation

Much has been said in recent times about the ever-increasing need for greater energy supply to meet the growing demand from power-hungry technologies like data centers, artificial intelligence (AI) and electric vehicles (EVs). But how are we faring in the...

Transforming the Petrochemical Landscape

The global energy industry is undergoing a dramatic shift as traditional refining processes evolve to meet the burgeoning demand for petrochemicals while contending with price volatility and environmental mandates. Navigating Global Energy Market Fluctuations The energy sector is no stranger...

Transitioning to Sustainable Power Generation: A Global Perspective

In recent years, the transition to renewable energy has become a central focus for nations across the globe. This movement is driven by the urgent need to address climate change, reduce carbon emissions, and meet the growing energy demands of...

Examining Volatility in the Energy Markets

Introduction In this technical briefing, we aim to provide an update on key Oil and Gas market indices and discuss whether we have moved past the significant volatility experienced between 2020 and 2024, or if the uncertainties persist in the...

Deep-Sea Mining – Panacea or Problem?

For quite some time now, much has been said about the world’s move toward clean energy and the goal toward net zero by 2050. To achieve this, demand will continue to grow for certain critical minerals, such as lithium, nickel,...

How is Electrification Disrupting the Energy Sector?

One of the biggest trends shaping society today is the widespread adoption of Electric Vehicles (EVs). While Tesla pioneered this movement as a disruptor, nearly every automobile manufacturer worldwide is now actively developing its own electric vehicles. Governments have implemented...

Carbon Capture – Is it Really Going to Materialise?

Before we discuss the carbon capture process and how it is used, it is worthwhile conceptualising the carbon emissions emitted worldwide and why different technologies, including carbon capture, must be considered as part of the energy transition. As can be...

Natural Gas – The Past, Present and Future

There has been a significant push towards transitioning to cleaner and renewable energy sources, moving away from fossil fuels due to their environmental impact. By looking at the past, the present and the future, the question remains: can we realistically...

High Grade Ore And A Question Of Indemnity

When a mine suffers business interruption, the issue of high grading can come into play. The question is whether insurers should actually benefit? Mining business interruption insurance and the principle of indemnity is no simple matter. Take the case of...

Recognition of Lost Production at a Gold Mine

With any loss measurement, we must understand how the incident impacted operations. In mining losses, this is no different, we need to understand both mining and milling operations. So, when there is an incident at a mine, how does this...

Renewable Energy Losses – Winds of Change

It is May 20, 1899. New York City taxicab driver Jacob German is the recipient of the United States’ first-ever speeding ticket. He whizzed by at 12 miles per hour on Lexington Avenue and was then pursued and remanded by...

Losses")

Biomass (Co-Generation) Losses

Certain agricultural entities can generate energy from the organic matter derived from their production process. This type of co-generation of energy is referred to as biomass energy. These biomasses can be agricultural in nature, as in the case of sugarcane...

Variable Mining Costs – How Should They Be Treated?

Variable expenses: one would consider this to be one of the easier aspects in the analysis of a mining claim; however, that is far from the truth. When it comes to mining losses, the determination of which costs are considered...

The Effect of Volatility on Power Generation Business Interruption Losses

It is clear to the casual observer that many aspects of the economy are facing volatility. Fuel, energy, labor, shipping - all have experienced unprecedented shortages and price increases because of a myriad of conditions. The Russia-Ukraine war, Covid-19, inflation,...

Upstream Oil and Gas Losses

In this briefing, we discuss various considerations in upstream oil and gas production losses, and in particular how rates of production depend on the type of well. We also discuss what the shift to horizontal drilling and hydraulic fracturing means...

How is the Power Generation Landscape In Canada Evolving and What Are The Challenges It Faces in the Near Future?

Canada is a world leader in power generation as it pertains to sources that do not emit greenhouse gasses. At the current moment, 83% of generation comes from non-emitting sources. Canada’s goal by 2030 is to have 90% of power...

Back to Coal mining in the UK, what about the risk, which risk?

If you have an interest in energy, heavy industry or simply ESG you cannot fail to have seen the news towards the end of last year - that the UK has approved its first coal mine for many years. The...

Waste to Energy

What is Waste to Energy? Waste to energy refers to the process of converting municipal solid waste (MSW), otherwise known as trash, into usable heat, electricity, or fuel. The three main MSW categories include: Biomass or biogenic (plant or animal...

An Introduction to Natural Gas: Separation, LNG and GTL Plants

Our first technical briefing introduced the Oil & Gas value chain, divided into: i) upstream; ii) midstream; and iii) downstream. Here is a recap, before we explore natural gas in more detail. Upstream: this involves the exploration and extraction of...

Imbalance of Gas Supply

The sanctions imposed on Russia amid the Russia-Ukraine conflict have impacted global gas markets, particularly those in Europe. Russia is the second largest producer of natural gas globally and used to supply about 40% of Europe's natural gas. However, supplies...

Mining BI Insurance: Remediation and Rehabilitation

All mines, no matter how vast or intricate, are ultimately temporary and will one day be depleted. When all valuable materials are extracted, or at least those that are cost-effective, mining operations will cease, and the mine will be decommissioned....

Renewable Energy Certificates

Since 1978, American regulators and policymakers have looked to incentivize the investment and development of generating renewable energy. Individual states began enacting Renewable Portfolio Standards (RPS) to support this mission by requiring a specific percentage of a utility’s energy portfolio...

Mining BI Insurance: Depreciation, Depletion and Amortization

The use of depreciation, depletion and amortization (DD&A) is an accounting method that allows the cost of an asset to be recorded as an expense over a period of time in order to reflect the use and consumption of the...

Potential Quantification Issues for Losses Involving Wind Farms Under Construction

Quantifying the financial impact stemming from the failure of an already commissioned single stand-alone wind turbine generator presents challenges, but these challenges increase exponentially when the failure occurs at a wind farm under construction. Additional complexities surface to the extent...

The Global Energy Crisis

As the Ukrainian conflict unfolds, Europe’s energy dependence on Russia becomes an increasingly critical bargaining tool. The economic sanctions imposed by some Western nations in response to Russia’s invasion appear to be increasingly directed against Russian oil and gas supplies...

Measuring Refining Margins for a BI Loss

When it comes to Business Interruption policies for Oil & Gas risks, there are different types of coverage available in the market, including Gross Profit, Gross Earnings, Specified Standing Charges etc. Common Policy Wordings Gross Profit equates to Turnover less...

The Importance of Mining Plans

Any well-run business starts with a plan, and a mining operation is no exception. Plans and budgeting or forecasting allow management to prepare for a future period, whether in the short-term or in the long run. Based on projections, management...

in Refinery Claims")

The Importance of Linear Programs (LPs) in Refinery Claims

The use of Linear Program models is common in refining, and other industries, to optimise their activities by using an algorithm subject to a set of inputs, constraints, and relationships. This article discusses the LP models in more detail and...

What Happened to Jet Fuel During Covid-19?

The main types of jet fuels used by airlines are Jet A-1, Jet A and Jet B. Jet A is mainly used in the United States, whereas Jet A-1 is commonly used outside the United States and Jet B is...

Mining BI Insurance and the Impact of Changes in Ore Grade

Ore grade refers to the metal content of an ore deposit, and it is the value of the contained metals or minerals less the cost of extracting and refining that drives the economics of a mine site. There can be...

A Lightning Fast Intro to Energy Market Basics

The summer has come to an end in Florida. Temperatures are still hot, and the afternoon thunderstorms are raging. So, when I open my electricity bill and gasp at the month’s cost, muttering some hopeless comments about how I should...

The Recovery of Oil & Gas: A Roller Coaster Ride or Merely a Few Speed Bumps?

Covid-19 has led to major disruptions across various sectors and the petroleum industry is no exception. Demand for oil and petroleum products, in general, declined due to reduced economic activity as governments worldwide imposed lockdowns and tightened border controls. Certain...

What Triggered the UK Energy Market Crisis and What is the Impact on BI Claims?

The UK’s energy wholesale markets have reached new highs, with daily average electricity prices rising above GBP 150 per MWh since early September 2021. A record high of GBP 424 per MWh, since at least January 2019, was reached on...

Introduction to the Oil & Gas Value Chain

The Oil and Gas industry in the insurance market is usually categorised between Onshore/Offshore or Upstream/Downstream. It includes a chain of businesses relating to extraction, transportation, refining, petrochemical and chemical – essentially from the carbon in the ground to the...

Regulated and Deregulated Electricity Markets: What is the difference when modelling power generation losses?

Introduction When modelling power generation losses for Business Interruption (“BI”) or Delay in Start-Up (“DSU”) purposes, it is important to understand the type of market(s) the Insured participates in and specifically how it operates within those markets. In this introductory...

Mining Claim – All Is Not As It Appears

In this briefing we focus on mining claims, and share our knowledge and technical expertise on one of the loss measurement issues regularly encountered in mining claims, production bottlenecks. What you will learn from reading the article include: How the...

Mining Business Interruption Insurance and the Principle of Indemnity

Mining Business Interruption Insurance and the Principle of Indemnity A contradiction? How can a mine claim for lost production when the ore is not lost and will be mined? Why does a mining company need to purchase business interruption insurance...

The Effect of Deductibles & Policy Wording – Is It What You Think?

With a typical Energy claim standing at approximately USD 4.5 million, it’s no surprise that Business Interruption (BI) is once again the #1 business risk for the fourth year in a row[i]. To help insurers mitigate their exposure when an...

Court Breaks with Apportionment

The case of Varco Canada Limited v. Pason Systems Corp., 2013 FC 750 (CanLII) involved an award of over $52M based on an accounting of the defendant’s profits. Perhaps more importantly, the decision sheds light on a number of conceptual...

Mining Industry Revisits Anti-Corruption Procedures

Mining companies should take note of Canada’s stricter penalties and more aggressive enforcement of anti-corruption laws and make sure their anti-bribery compliance procedures are up to speed, lawyers, forensic accountants and mining executives warned at a recent conference in Toronto....