The Dividend Double Count

01 September, 2015

01 September, 2015-

Ephraim Stulberg

Ephraim Stulberg -

Canada

Canada

In this post, I touch on a common error I encounter in dealing with a financial analysis of multiple companies owned by the same group or individual. I call this error the “dividend double count”, for reasons that will become apparent momentarily. The error arises in various areas of my practice, but most commonly in the areas of family law and personal injury.

The Issue

The error is as follows. Consider the following simple ownership structure:

Now, suppose that during the most recent calendar year, the following results were reported:

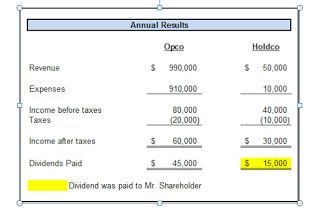

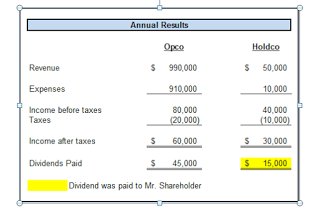

The question that arises in a family law context is: what was the pre-tax income available to Mr. Shareholder? An intuitive response might be to simply look at the “income before taxes” line on the income statements of Opco and Holdco, and take the sum of $120,000 (i.e. $80,000 + $40,000). Some may also be tempted to pick up the $15,000 in dividends paid to Mr. Shareholder.

But this would be wrong.

Opco shows dividends paid of $45,000. Holdco is the sole shareholder of Opco, so those dividends – which have not been deducted in calculating Opco’s income before taxes – are appearing as part of Holdco’s revenue (along with some miscellaneous revenue).

Had Opco paid out a $45,000 management fee to Holdco, the analysis would be much simpler; the management fee would show as an expense to Opco and as revenue to Holdco; the impact on the combined net income of the two companies would be neutral. The problem really arises because dividends are not deducted in calculating income. In order to calculate the overall pre-tax income, it is necessary to deduct the $45,000 in intercompany dividends. The actual pre-tax income of the two corporations is $120,000 – $45,000 = $75,000.

(The same commentary would apply to the $15,000 reported by Mr. Shareholder on his personal tax return; these have been paid out of Holdco’s pre-tax income, and should not be included again at the personal level in analyzing Mr. Shareholder’s income).

Other Contexts

This issue also arises in other situations. A number of years ago I analyzed the income of a group of real estate development companies in the context of a claim for personal injury damages. The plaintiff’s expert had presented a claim based on a decline in net income between the pre-accident and post-accident periods, but had neglected to consider the distortions created by the issuance of large intercompany dividends.

Conclusion

Dividends issued from one company to another are included in the income of the recipient, but are not deducted from the income of the issuer.[1] In analysing the revenue or profitability of a group of companies, it is important to gain an understanding of how the revenue of each company is generated in order to gain a proper picture and to avoid double counting.

By Ephraim Stulberg.

The statements or comments contained within this article are based on the author’s own knowledge and experience and do not necessarily represent those of the firm, other partners, our clients, or other business partners.

The Income Tax Act recognizes this; intercompany dividends amongst related companies are not subject to tax in the hands of the recipient company.

Ephraim Stulberg

B.A, M.A, M.BA, CPA, CA, CBV, CFF, Partner/Senior Vice President

- +1 416.366.4968

- estulberg@mdd.com

- Toronto, ON, Canada

Articles

Relevant Articles

Our experts are extremely knowledgeable about thier subject areas and often write educational material and commentary on topical issues they come across.

Ghosts, Ghouls and Cyber Claims

We usually think of Hallowe’en when October rolls around; however, did you know that October is also cyber security awareness month? NetDiligence recently released the 12th iteration of their Cyber Claims Study. They analyzed approximately 7,500 cyber claims from period...

ESG Disputes and Business Valuation

Environmental, Social and Governance (“ESG”) factors have gained increasing importance in recent years as society has become more aware of how corporate conduct affects stakeholders, the environment and humanity at large. From issues such as climate change to socially responsible...

Business Valuation, Growth Rates and Climate Change: a Case Study of Vail Resorts

This past summer’s heatwaves and wildfires served for many as alarming reminders of climate change. Hotter summers, colder winters, and more hurricanes are amongst the symptoms of a changing global climate[1]. These climatic effects will impact different businesses in different...

COVID-19’s Impact On Business Valuation

This is the second blog post co-authored by MDW Law Partner, Christine Doucet, and MDD Forensic Accountants Partner, Jarrett Reaume, addressing various aspects of COVID-19’s impact on business owners and family law issues. Their first blog post was “Guideline Income...

Is Kylie Jenner a Billionaire, or Even Close? Part III

I hope this will be the final installment in this series, but one never knows. Back in the summer of 2018, I wrote a short piece questioning a sensational Forbes magazine article claiming that Kylie Jenner was worth $1B, based mainly...

Is Kylie Jenner a Billionaire, or Even Close? Part II

A little over a year ago, I wrote a short blog post taking issue with a Forbes magazine article that had concluded that Kylie Jenner's net worth was around $900 million. In light of last week’s news that Coty Inc., a publicly traded cosmetics firm, is...

Buying Shares in an NFL Player? Business Valuation Principles Still Apply

In my last post, I argued that an investor in Kylie Jenner’s cosmetics company was essentially investing in Ms. Jenner’s personal brand, and that the earnings stream for that brand was of a finite life. The post got me thinking:...

Is Kylie Jenner Really a Billionaire, Or Even Close?

A few weeks ago, Forbes created a social media storm when it proclaimed that Kylie Jenner was poised to become the world’s youngest self-made billionaire. Many thumbs were worn out debating the appropriateness of the term “self-made”, and apparently a GoFundMe page...

Valuing a Franchise System

Valuing a franchise system, or “franchisor”, is in many ways very similar to the valuation of any other type of business; it is a function of the forecasted levels of cash flows that the business will generate, and the risk...

How Much Is Your Business Worth?

As a Chartered Business Valuator (CBV), almost every business owner I meet wants to know the answer to this question: “How much is my business worth?” There can be many reasons for asking this question: they may be planning to...

What Type of Business Valuation Do I Need?

In my previous article, I discussed the critical need for business owners to have their business valued by a professional appraiser. In this article I will discuss the two types of business appraisals that you might want to consider. Calculation...

Should I Have My Business Valued?

What's so important about having a valuation of my company? Small business owners spend most of their time IN THEIR business and not ON THEIR business. Further, they view expending money on getting a professional valuation performed as a completely...

Identifying and Measuring Short Duration Business Interruption Losses

What have we really lost? One of the most common issues that arise from short-duration interruptions, those measured in days as opposed to weeks or months, is whether the business actually suffered a permanent loss of revenue or whether the...

Business Valuations & Why It Pays To Use Genuine Experts

The Basics Assets have value if they will give rise to future economic benefits. For businesses, these future economic benefits take the form of either the expected net income stream or the amount that could be realised in the short...

Gift Cards and the Illiquidity Discount – A Valuation Perspective

With the busiest season of the year for retail sales upon us, you are no doubt wondering what to buy for that special someone. If you’re reading this blog – and I have every reason to believe you are –...

I Lost My Customers and It’s Your Fault!

In Schwartz Levitsky Feldman LLP v. Werbin, 2015, an action was put forward by Schwartz Levitsky Feldman (SLF) claiming loss of profits due to the departure of Mr. Werbin. The firm contended that they purchased Werbin’s clients when they purchased...

The Dividend Double Count

In this post, I touch on a common error I encounter in dealing with a financial analysis of multiple companies owned by the same group or individual. I call this error the “dividend double count”, for reasons that will become...

Adding up the Damage: Lost Profits vs. Business Value

When a business is destroyed as a result of wrongdoing, there are two commonly used methods by which the plaintiff’s damages may be measured. One method is to appraise the value of the plaintiff’s business at the date of loss;...

Calculated Risk: A $75M Award Adds Urgency to Pre-Judgment Interest Considerations

Pre-judgment interest is often the last thing litigants ponder. A recent award of $75 million in pre-judgment interest in Eli Lilly v. Apotex, 2014 FC 1254 (“Cefaclor”) may change that. Cefaclor involved the infringement of patents for an antibiotic. Damages...

Personal Injury Losses and the Self-employed: A Business Valuation Perspective on Labour & Capital

Business valuation concepts can be critical for the proper quantification of personal injury damages, particularly in the context of self-employed individuals. Business valuators are commonly called upon to assess the fair market value of small, owner-managed businesses. One of the...

5 Ways You Should Be Using Your Financial Expert

Moore v. Getahun 2015 ONCA 55 is a case that has already generated a lot of discussion and navel gazing in both the legal and expert communities, and I hesitated for quite a while before deciding that I had anything worthwhile to...

Dunkin’ Donuts c. Bertico inc., Part II: Lost Profit & Loss of Business Value

Towards the end of its decision in Dunkin’ Brands Canada Ltd. c. Bertico inc.2015 QCCA 624, the Quebec Court of Appeal discussed the issue of whether an award for both a) lost profits up to 2005 and b) loss of business...

Untying the Knot: A Forensic Accountant’s View of Divorce Proceedings

During the course of matrimonial disputes, there are often situations where solicitors find it helpful to engage specialist investigators and appraisers. In particular, forensic accountants can help to provide the court with a clearer view of the true financial position...

Accounting For Attorneys

It is becoming increasingly important for attorneys to understand financial statements and their relevance to various types of business and legal situations. The non-accountant attorney will greatly benefit from a basic understanding of the key principles of accounting. Equally important...

Business Valuations: When You Would Need One

Business valuations in one form or another have been around for decades. As a result of the Eighteenth Amendment to the United States Constitution, the Internal Revenue Service began issuing memorandums and directives relating to methods for determining values and...